The Ultimate Overview Of Tokenization Platforms Ecosystem

Key Takeaways

- The hardest part of tokenization is not minting the token but handling compliance, identity, transfer restrictions, sanctions, and corporate actions across jurisdictions and chains. No single standard has won outright because the real prize is not the standard itself, it is owning the reference implementation that everyone else builds toward.

- The RWA tokenization market is splitting into four distinct operating models, and the strategic tradeoff is the same across all of them: the more control and compliance you build in, the harder it becomes to plug into DeFi. The platforms that crack that tension will define the next phase of the market.

- Every major architectural decision in tokenization flows from one question: where does the compliance logic live? Inside the token, outside it, or at the network layer. That single design choice determines gas costs, upgradeability, cross-chain portability, and DeFi composability downstream.

- Tokenized T-bill deposits on Morpho fell 92% while tokenized gold grew 7x over the same period. Onchain allocators are already rotating across RWA collateral based on macro conditions, which is behavior that looks a lot more like institutional portfolio management than crypto speculation.

- RWA activity in DeFi is heavily driven by leveraged looping strategies, and that is not a caveat, it is the signal. Posting a tokenized asset as collateral, borrowing against it, and redeploying in a single automated workflow is exactly the kind of capital efficiency traditional finance has wanted for years but could never operationalize this cleanly.

Sign up for TokenizeThis NYC — a three-day tokenization conference, June 23-25 2026, and join us at the eth.cc TokenizeThis event.

Featured Projects and Organizations

Contributors

RedStone, as the main author of the report, would like to express true gratitude to all the contributors, projects, and key opinion leaders who helped us create such a comprehensive piece on the yield-bearing assets landscape. Starting with big gratitude towards Gauntlet and Dune teams, especially the research department, for their diligent and timely work. The depth and breadth of this report wouldn’t be possible without these individuals. Special thanks to Securitize, Centrifuge, Superstate, Ondo, Spiko, WisdomTree teams and multiple other kind contributors to the final report.

| Tokenization Ecosystem Overview | ||||

| Tokenization Platforms | Tokenized RWAs | DeFi Protocols | ||

| Securitize | Tokeny (Apex) | BlackRock (BUIDL, CASH) | Apollo (ACRED, ACRDX) | Morpho |

| KAIO | Theo | VanEck (VBILL) | Hamilton Lane (SCOPE) | Aave Horizon |

| Centrifuge | Libeara | Franklin Templeton (BENJI) | Ondo (USDY, OUSG) | Euler |

| Spiko | Ondo | Superstate (USTB & USCC) | Spiko (EUTBL, USTBL, C&C) | Pendle |

| Superstate | Figure | Wisdomtree (WTGXX) | Wellington Management (ULTRA) | Kamino |

| WisdomTree | Hadron Tether | Maple (syrupUSDC) | Fidelity (FDIT) | |

| Midas | Janus Henderson (JTRSY, JAAA) | Tether Gold (XAUT) | ||

Join The Low-Risk DeFi Movement 📊

What Is Tokenization And How It All Started?

Tokenization refers to the process of converting rights to real-world assets (RWAs)—such as currencies, bonds, equities, real estate, commodities—into digital tokens on a blockchain. These tokens represent ownership or fractional shares, enabling seamless trading, enhanced liquidity, transparency, and accessibility without traditional intermediaries. By leveraging distributed ledger technology, tokenization democratizes investments, reduces transaction costs, and facilitates 24/7 global markets. It bridges traditional finance (TradFi) and decentralized finance (DeFi), unlocking trillions in previously illiquid assets.

True tokenization emerged with Ethereum in 2015, which introduced programmable smart contracts and the ERC-20 standard, becoming the “universal language” for fungible tokens. This enabled the tokenization of RWAs beyond cryptocurrencies.

2014. Tether launches USDT, the first major stablecoin, proving RWAs could be issued, transferred, and used at global scale — creating the foundational onchain dollar that powers everything else.

2018. Circle launches regulated USDC with transparent reserves, establishing institutional-grade compliance and trust standards that become the preferred settlement and collateral layer for all future RWAs.

2020. Centrifuge launches Tinlake alongside DeFi Summer, turning stablecoins into productive collateral and originating the first onchain private credit — birthing real yield and the entire RWA lending market.

2021. Franklin Templeton launches BENJI, the token for U.S. Government Money Market Fund (FOBXX), the first U.S.-registered mutual fund on a public blockchain, showing regulated TradFi products could run natively onchain with daily liquidity and redemption — opening the institutional floodgates.

2023. Ondo launches OUSG tokenized short-term Treasuries, bringing verifiable institutional-grade yield onchain for the first time and igniting the tokenized cash & fixed-income boom.

2024. BlackRock launches BUIDL on Ethereum through Securitize, delivering irreversible credibility and billions in AUM as the world’s largest asset manager enters tokenized funds — mainstreaming RWAs overnight.

2025. Tokenized equities and ETFs scale through platforms like Backed (xStocks) and Ondo Global Markets, expanding RWAs beyond fixed income into real stocks and enabling 24/7 trading, fractional ownership, and full DeFi composability.

2026. WisdomTree receives SEC approval for 24/7 trading and instant USDC settlement of its tokenized MMF (WTGXX), becoming the first registered fund with true secondary-market liquidity under U.S. rules — shifting the entire vertical from issuance to live, tradable infrastructure.

Key Considerations For Tokenization Standards

Tokenization as a concept might sound deceptively simple. You take a real-world asset, a stock, gold, a bond, real estate, and represent it on a blockchain ledger. Easy, right? Not quite.

There is broad consensus in the industry that properly tokenizing an asset is significantly harder than building on top of natively onchain assets. The complexity runs deep, spanning multiple implementation layers:

- Compliance

- Security

- Whitelisting

- Identity and investor verification

The assets being tokenized here are predominantly securities, and as such they must adhere to securities law, not only in the jurisdiction where they were issued, but also in every jurisdiction where investor capital is accepted. That alone creates enormous legal and technical overhead. Transfer rules are a direct derivative of this compliance challenge. And the problem compounds further when you consider that issuance rarely happens on a single chain. The moment a tokenized asset needs to exist across multiple networks, you inherit an entirely new layer of risk: ensuring that cross-chain bridges are secure, and that the token supply, ownership records, and transfer restrictions remain correctly accounted for across every chain it touches. Add corporate actions on top of all that, and the picture gets considerably more complex.

The core tension here is that there is no single tokenization solution that fits all cases. Yet paradoxically, many major players in the space are deeply invested in becoming the author and canonical owner of the standard everyone else ends up adopting, even though most of these standards tend to be open source with permissive licenses by the time they reach broad adoption. This mirrors a dynamic well understood across open source software: owning the reference implementation of a standard, even a freely available one, generates powerful product and brand flywheel effects that are hard to replicate any other way. We will dig into those dynamics shortly.

But first, let’s walk through the most prominent tokenization standards in use today, their distinct features, architectural approaches, and the teams behind them.

| Provider | Identity Model | Transfer Compliance | Sanctions | Corporate Actions | Chains |

| Open Standards | |||||

| ERC-3643 (T-REX) | onchain identity contract per investor; claims portable across all EVM chains | Modular rule engine embedded in token; all rules must pass; configurable at runtime without redeployment | Claim revocation by issuer; transfer auto-fails on next attempt | No native support; external contracts required | Any EVM chain |

| ERC-1404 | None defined; issuer manages their own allowlist | Two-function check: restriction code and reason string; compliance logic lives outside the token | Issuer-defined; typically off-chain removal from allowlist | None native; composable externally | Any EVM chain |

| Token-2022 | Accounts frozen by default; KYC-verified accounts thawed; supports Civic Pass and Solana Attestation Service | Real-time check via Transfer Hook; includes Permanent Delegate for issuer-forced transfers | Sanctions check runs inside hook program; note: Transfer Hook and Confidential Transfers cannot be active on the same token | Interest-bearing extension for yield accrual; Scaled UI for rebase display; hooks can encode corporate action triggers | Solana |

| Proprietary Protocols | |||||

| Securitize DS Protocol | Investor-centric: many wallets map to one investor ID; individual onchain vault per investor for DeFi (from 2026) | EVM: restricted ERC-20; Solana: Token-2022 Transfer Hook + Permanent Delegate enforcing DS compliance logic natively | Off-chain compliance screening + onchain revocation; SEC-registered transfer agent | V4: real-time onchain rebasing for yield + corporate actions; EIP-712 investor self-whitelisting; SEC-registered transfer agent for distributions, voting, record dates | Multiple EVMs, Solana, Aptos and Algorand |

| Ondo Global Markets | Global Markets tokens are available globally, subject to certain jurisdictional restrictions, including those based on securities laws and sanctions requirements. Persons in the United States are not able to subscribe for or redeem Global Markets tokens. | Global Markets tokens trade on permissionless, public blockchains. | Global Markets tokens are monitored through real-time blockchain analytics. | Dividends auto-reinvested and reflected in token price | Ethereum, BNB Chain and Solana |

| Spiko | PermissionManager contract uses bytes32 bitmasks for up to 256 groups. NAV is calculated by CACEIS and brought on-chain via oracles. | Strict allowlist check on every transfer. Redemptions route via a dedicated contract, where requests are batched, processed, and burned daily. | Handled via off-chain AML monitoring by the fund admin. Enforced by revoking allowlist status. | Funds are accumulating (no discrete dividend distributions). Daily yield is reflected directly in the token price via a daily on-chain NAV heartbeat. | Multiple EVMs, Starknet, and Stellar. |

| Superstate | Entity ID groups multiple wallets per investor; per-fund permission flags on allowlist contract | EVM: allowlist check per transfer; Solana: Token-2022 freeze/thaw — thaw is permissionless so DeFi protocols can onboard users directly | Off-chain KYC + onchain allowlist revocation; SEC-registered transfer agent | Funds: Daily 3rd-party NAV with per-second yield accrual; Stocks: Real-time public exchange pricing with discrete dividends; SEC-registered transfer agent for all. | Ethereum, Solana, Plume; |

| KAIO (prev. Libre) | Onchain Investor Registry with attested credentials; configurable three-tier rules: protocol, fund manager, and fund level | Phase-gated order books; modular multi-tier rules enforced per operation; onchain attestations at every gate | Off-chain compliance checks with attested credentials per operation; onchain revocation | Full fund lifecycle via phase-gated order books; NAV-based pricing and configurable execution windows | Any EVM chain, Sui Aptos, Hedera, Solana |

| Centrifuge | SEC-registered transfer agent handles KYC; pluggable transfer hook system with four compliance modes (FreelyTransferable, FreezeOnly, RedemptionRestrictions, FullRestrictions) configurable per share class; membership expiry and freeze state encoded per investor; burn-and-reissue for wallet recovery | ERC-1404 (EVM token layer); hub-and-spoke multichain with multi-adapter quorum consensus (Wormhole, LayerZero, Axelar, Chainlink); configurable threshold (e.g. 2-of-3) per chain-pair and per pool; recovery adapter for emergencies; per-pool issuer configuration, isolated across pools | Transfer agent revocation; off-chain process; SEC-registered transfer agent | NAV-based pricing per epoch; all corporate actions via SEC-registered transfer agent | Ethereum, Base, Arbitrum, Avalanche, Plume, BNB, Optimism, HyperEVM, Monad (9+ EVM chains), Solana, Stellar |

| WisdomTree | Stellar: issuer must approve every transaction at network level — no smart contract required; Ethereum: DTCC-managed allowlist | Stellar: Protocol-level gate; Ethereum: DTCC-synced allowlist via Token Factory | Issuer-controlled; off-chain KYC and network-level controls on Stellar | onchain dividend reinvestment via USDW stablecoin; investors elect to receive payouts in digital form | Multiple EVMs, Stellar and Solana |

Note: Token-2022 is Solana’s native token extension framework and serves as the underlying infrastructure for multiple distinct issuers operating on the network, including Securitize, Superstate, and Ondo. It is covered separately here to document the foundational technical capabilities it provides, independent of any single issuer’s implementation choices.

KYC & Identity: Who Gets to Hold the Token?

Every permissioned token needs to know, at the moment of transfer, whether both the sender and the receiver are allowed to hold it. KYC verification happens off-chain, but how its result is represented onchain varies significantly across standards and shapes most of your architecture.

ERC-3643 solves this with a portable identity layer: every investor gets their own onchain identity contract, carrying verified claims about who they are. The same identity works across every Ethereum-compatible chain, so an investor verified once is recognised everywhere. Securitize takes a different angle, focused on a specific regulatory constraint. US securities law introduces registration requirements at around 2,000 holders, so Securitize groups multiple wallets under a single investor IDand, from 2026, gives each investor a dedicated onchain vault so that beneficial ownership stays traceable even inside DeFi protocols.

Most production deployments use a simpler model: a managed list of approved wallet addresses. Spiko, Superstate, KAIO, Centrifuge, and WisdomTree on their EVM deployments all follow some version of this pattern. It is fast and cheap, but tied to each issuer individually. WisdomTree on Stellar and Token-2022 on Solana push compliance to the network layer itself, where accounts are locked by default and only activated once KYC clears.

Transfer rules: What Happens at the Moment of Transfer?

Knowing who can hold a token is one problem. Deciding what happens when a token actually moves is another. The logic could live inside the token, outside it, or be delegated to the network entirely, and each choice involves a different tradeoff between flexibility, cost, and composability with DeFi.

ERC-3643 builds the rules directly into the token as a modular engine. Issuers can add or remove rules, jurisdiction blocks, holding limits, lock-up periods, without redeploying anything. KAIO uses standard ERC-20 tokens with compliance enforced by a separate onchain protocol engine, preserving full composability with wallets, custody providers, and DeFi infrastructure while applying institutional-grade transfer restrictions. Rules are configured across three tiers: protocol, per-fund manager, and per-fund. Distributors operate within these rules. The richness comes at a cost: transfers consume more gas than a standard token move.

ERC-1404 goes the opposite direction. The token only defines two things: a restriction code and a human-readable reason. All the real logic sits outside, in a contract the issuer can upgrade independently. It is the approach Centrifuge uses at the EVM layer, keeping the token clean while the compliance infrastructure evolves separately. Most other platforms use a restricted ERC-20 that simply checks an allowlist on every transfer. On Solana, Token-2022 handles this through a hook program that fires on every transfer and can run any logic the issuer defines, fully decoupled from the token itself.

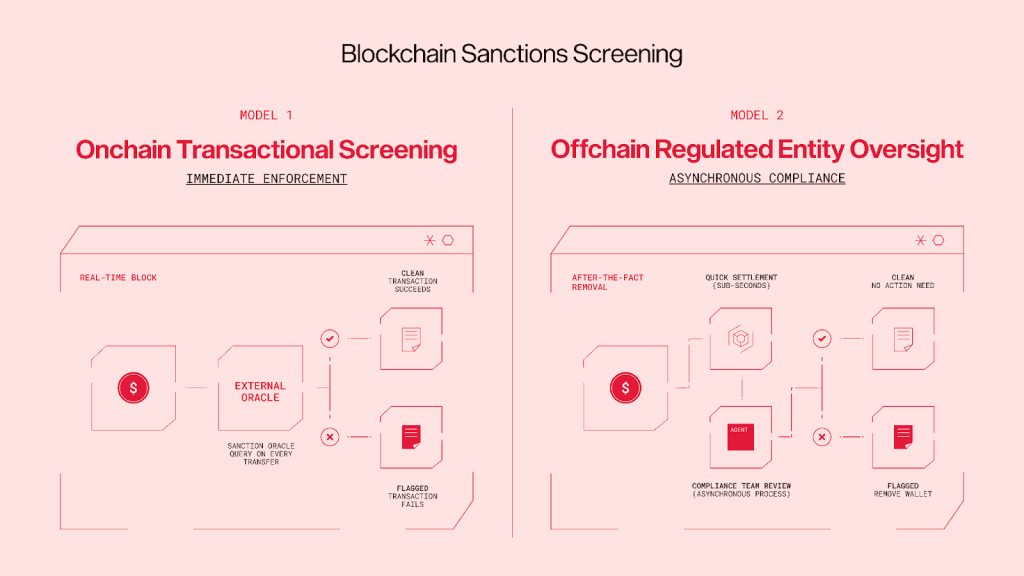

Sanctions & holding restrictions

Sanctions are a timing problem. Most blockchains settle in sub-seconds, while a sanctions designation happens through a legal and regulatory process that runs asynchronously. Every platform has to decide: enforce the block onchain the moment it is known, or rely on a compliance team to remove wallets after the fact.

ERC-3643 takes a softer approach: when a KYC claim is revoked, the next attempted transfer fails automatically. There is a short window of exposure, but the mechanism handles any compliance event, not just sanctions.

Everywhere else, the responsibility sits with a regulated entity. Securitize, Centrifuge, and Superstate all operate as SEC-registered transfer agents, meaning their compliance teams carry legal accountability for sanctions screening, which is arguably more robust than any automated oracle. Similarly, Spiko acts as a transfer agent to handle its own sanctions screening, operating under the supervision of the French AMF alongside its regulated fund administrator The practical case for this model is straightforward: onchain enforcement is only as good as the data feeding it, whereas a regulated entity is directly accountable for getting it right.

Corporate Actions: Dividends, Splits, and Redemptions

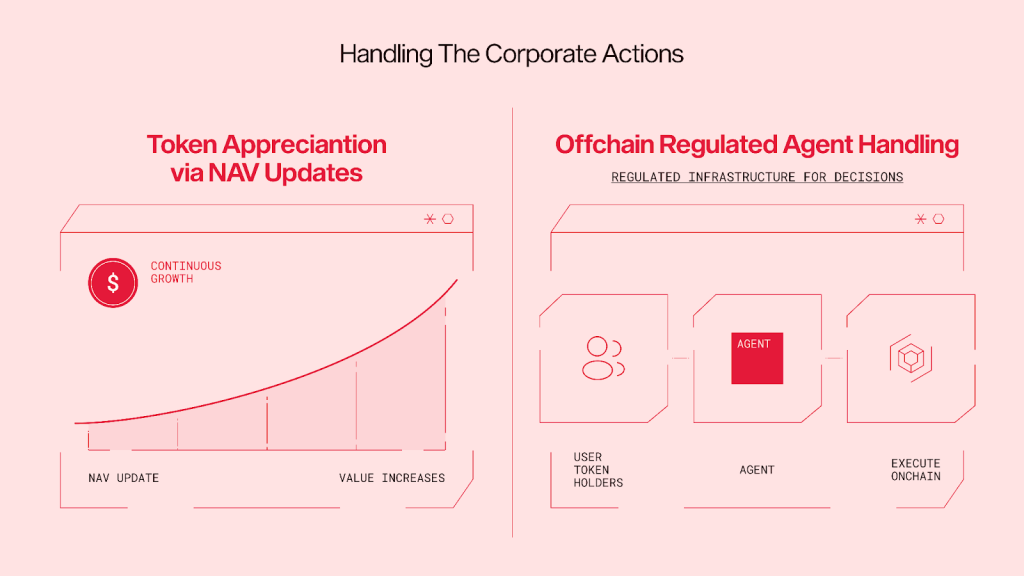

Corporate actions are where tokenisation promises the most and, so far, delivers the least on the smart contract side. Automatic onchain dividends, programmatic voting, atomic splits—these were the headline promises. In production, the most sophisticated deployments have moved this complexity off-chain into regulated infrastructure.

For yield-bearing funds, the cleanest solution is encoding returns in the token price rather than distributing them as events. Spiko updates NAV daily through its regulated fund administrator. Superstate pushes this further with a continuous oracle updating every second. Centrifuge batches all deposit and redemption requests into epochs. At epoch close, the pool manager approves orders at the current NAV, shares are issued or revoked with balanced accounting entries, and fulfillment callbacks are sent cross-chain to each spoke where investors can claim. This epoch-based order processing eliminates the cash-drag problem the report discusses in Part 2: redemptions are processed at verified NAV without requiring idle liquidity buffers.There are no distribution events, just a token worth more over time. Ondo handles equity dividends by automatically reinvesting them into the reference stock, with the effect reflected in the token price. WisdomTree built an onchain reinvestment mechanism where fund investors can elect to receive payouts in their own USDW stablecoin.

Securitize’s DS Token v4 advances this by introducing a native rebasing mechanism, allowing dividends and splits to be executed as single onchain state changes across all holders. For everything else, votes, restructurings, tender offers, every major deployment routes through a regulated transfer agent. Securitize, Centrifuge, and Superstate all hold SEC transfer agent registration, handling corporate actions identically to traditional securities with onchain settlement at the end. The smart contracts handle token mechanics, the regulated infrastructure handles decisions.

Genuine onchain governance for tokenised securities at scale remains an open problem, and as of early 2026, no major deployment has meaningfully solved it.

Owning the dominant tokenization standard may not look like a competitive advantage on the surface, especially when the code is freely available to anyone. But the compounding effects run deeper than the license. The issuer that writes the standard sets the vocabulary and the integration target that everyone else builds toward. Every new deployment that adopts it validates the author’s infrastructure, pulls compliance workflows, identity systems, and service integrations into their orbit, and drives demand for their tooling.

The standard becomes the distribution channel. That is the flywheel.

Tokenization Ecosystem Overview Of Key Players

Tokenization isn’t one market but rather a multi-layer ecosystem. This is true of its participants, its applications, and the infrastructure supporting it all. Institutions, crypto-native firms, asset issuers, protocols, and service providers all play different roles in this evolving ecosystem and standards become increasingly important at the intersection of these roles and responsibilities. This applies to issuance, identity, transfer rules, reporting and compliance, pricing, collateral utility, liquidity, and composability, among others. 2025 was a year of consolidation through heavy investment and M&A activity, bringing together puzzle pieces that started building since tokenization’s early days in 2017/2018 (some even earlier), resulting in synergistic ecosystems meant to be greater than the sum of their parts. As those puzzle pieces come together it also means standards are put in place for compatibility across their ecosystem.

Tokenization Platforms Overview

| Platform | Focus | TVT | HQ | Key Partners |

| Securitize | Equities, registered & private funds, institutional DeFi | $3.3B | USA | BlackRock, Apollo, Hamilton Lane |

| KAIO | Tokenized funds, structured products, DeFi composability | $118M | Singapore | BlackRock, Brevan Howard, Hamilton Lane, Laser Digital |

| Centrifuge | Tokenized funds and DeFi infrastructure | $1.5B | Global | Janus Henderson, Apollo, S&P |

| WisdomTree | Tokenized funds and ETPs | $813M | USA | BNY, WisdomTree Prime & Connect |

| Superstate | Tokenized funds and public equities | $1B+ | USA | BNY Mellon (Custodian on USTB)Galaxy, Forward Industries, Sharplink (equities) |

| Ondo | Tokenized treasuries and equities | ~$2.6B | USA | Alpaca |

| Figure | Blockchain-native capital markets | $21B+ originated | USA | Jump Trading, BitGo, Sixth Street |

| Tokeny (Apex) | Enterprise tokenization infrastructure | $32B+ facilitated | Luxembourg | Apex Group, DTCC, AMINA Bank |

| Spiko | Tokenized UCITS money market funds | ~$1B | France | CACEIS, SG-Forge, Index Ventures |

| Theo | Full-stack tokenization with integrated liquidity | ~$200M+ | USA | Wellington Management, Standard Chartered, SIG |

Tokenization Platforms

These companies, often licensed in their respective jurisdictions and those they service, provide the operational layer for tokenization, including issuance, transfer controls, permissions, investor onboarding, and servicing and compliance workflows. With that in mind, tokenization platforms are growing beyond the minting and management of the token and into building with partners around it as this is where traditional fund management and blockchain-native market structure meet. This ranges from creating standards for and integrating DeFi vaults to working with distribution partners, and more.

Although standards may be created within different platforms and ecosystems, those players themselves diverge in strategy which makes sense given the various types of customers they could be going after. These are different operating models optimized for different levels of controls, compliance, interoperability, liquidity, and distribution. Some take the approach of making it as easy as possible for traditional asset managers to bring existing assets onchain. Others are building with portability and DeFi compatibility at the center, and some are looking to recreate entire capital markets natively on blockchain rails. The tokenization platforms covered in this report generally fall into one (or two) of these four categories:

- Manager-Controlled Tokenization Environments

- Institutional Operating Systems and Regulated Issuance Partners

- Standards and Compasibility-First Platforms

- Vertically Integrated /Blockchain-Native Capital Markets

Manager-Controlled Tokenization Environments

Examples: WisdomTree, Ondo

This first category is made up of asset managers and product issuers, building infrastructure to support their own products, clients, and regulatory responsibilities. In the buy, build, or lease question, these are the players that chose to mainly build. Rather than just relying on outsourced infrastructure providers they’re internalizing a lot of the tech and workflows themselves including subscriptions and redemptions, investor onboarding, permissions, and of course the investor experience. Tokenization is just a feature rather than the main focus here, where distribution is the broader strategy.

Control is the main advantage for this approach. The issuer owns both the funds/products and the infrastructure powering them, giving them the ability to customize token design and workflows to their target end investor, whether its retail or institutional. WisdomTree’s app ecosystem (Prime for retail, Connect for institutional) and Ondo’s split between institutional treasury products and more freely circulating global market tokens all reflect this logic.

Control and customizability come with a downside and in this case it’s deeper fragmentation. If every issuer builds its own access layer, standards, and redemption pathways then cross-platform interoperability becomes a bit more challenging and branded silos may begin to form. Nonetheless this may remain a popular approach for institutional issuers building in the space and seeing tokenization as an extension of product construction and client distribution.

Institutional Operating Systems and Regulated Issuance Partners

Examples: Securitize, KAIO, Superstate, Spiko

The platforms addressing institutional needs are the operational layers behind tokens issued by third parties. These are not asset managers themselves, they provide the tools for issuance of funds, equities, and structured products, their administration, permissions, and even distribution and DeFi utilization. The value-add here is providing the infrastructure for issuers that want to go to market onchain without having to build the rails themselves (the “lease” option of the “buy, build, or lease” question).

This has been one of the more successful models to bring institutions onchain as evidenced by Securitize who has served as the operational partner for some of the most recognizable issuers in the space, giving them the infrastructure to manage their tokens and building solutions to compliantly access DeFi. KAIO is also building for compliant access and lifecycle management for tokenized funds and structured products with integrations to other ecosystems through their Gateway. Superstate’s hybrid token and book-entry architecture allows for co-existence and investor choice. Meanwhile Spiko put strong emphasis on fund admin for tokenized money market funds using the blockchain as the registry of record. The common theme here is that beyond issuance, these platforms really become part of the operational fabric of the underlying assets.

Clearly this model works, lowering the barrier to entry for institutions while preserving the controls they require. However, there’s a caveat. This translates to priorities lying in restricted transfers, permissions, and reliability over unrestricted asset mobility. This means to access DeFi, for example, there needs to be custom solutions in place to account for those pillars including custom wrappers, curated standards, and close collaboration with partners for compatibility. This makes the model less open than purely crypto-native approaches, but also far more practical for institutions entering the market today.

Standards and Composibility-First Platforms

Examples: Centrifuge, Apex/Tokeny, Theo

The third approach emphasizes standards and interoperability. These platforms would see tokenization’s true value being realized when assets can move across other platforms, blockchains, and market functions. Rather than focusing mainly on fund administration or manager-controlled distribution, these players concentrate on standards, vault structures, liquidity architecture, and token design that enable tokenized assets to function within broader onchain financial systems.

Different platforms may go about it in different ways. Centrifuge is very explicit about the protocol-level standards they use and their vault infrastructure to make RWAs DeFi-ready from issuance, while also operating Anemoy as its institutional asset management arm, providing white-glove fund setup and management services that overlap with the Institutional Operating Systems category. What does standardization bring? It brings easier integration for lending, liquidity, and portfolio management. Tokeny on the other hand has a focus on the compliance side at the token layer through ERC-3643 and with their ONCHAINID for transfer restrictions. Theo looks at liquidity, market-making, and distribution as essentials for tokenization to flourish and therefore has them already integrated into the platform, making them product features rather than optional add-ons. The common theme here is that tokenized assets are treated as reusable financial primitives.

The main benefit here is that over time this approach will bring scalability through shared infrastructure. Building on standards and their frameworks makes these tokenized assets easier to integrate into other ecosystems. With that comes complexity in implementation of systems and therefore this is reserved for issuers who give the utmost importance to market utility rather than digitizing existing operations. This approach is what will drive market interoperability.

Vertically Integrated /Blockchain-Native Capital Markets

Example: Figure

Last but certainly not least, vertical integration is the most ambitious of the segments and therefore also less common. Rather than building one or some pieces of the tokenization stack, these players are building a whole capital markets system onchain across origination, issuance, trading, collateralization, securitization, secondary market infrastructure, and DeFi access. Figure is the go-to example here, owning the whole pipeline as they moved from blockchain-based lending into securitization (their HELOCs), yield-bearing cash products (YLDS), marketplace infrastructure (Figure Markets and Democratized Prime), and native public equities (OPEN).

This approach could lead to larger network effects rather than relying on the issuers or infrastructure providers. This is because there are less dependencies on third-party intermediaries and Figure in this case takes it upon themselves to power it all. At scale this can show what an institutional blockchain-based market infrastructure could look like, from start to finish. However not many will be taking this approach because of the biggest trade-off: execution. This approach requires expertise in multiple areas including regulation and market structure, product depth, access to liquidity, and traction. Again, not many will go after it but for those that can, it does provide the clearest picture of a truly onchain, fully-integrated market architecture.

Overall these four models show that the tokenization space is separating based on where participants believe value creation is concentrated rather than a single templated approach. The first model, manager-controlled environments, put strong priority on ownership of the product and client experience. The institutional operating systems are streamlining how third-party issuers can come onchain while preserving regulatory compliance and servicing workflows. Meanwhile those platforms focused on standards are making their assets usable across a larger selection of applications and environments. Vertically-integrated platforms have the heaviest lift as they look to build financial systems entirely onchain.

These models aren’t mutually exclusive, some of the platforms actually approach tokenization using a blend of some of these models. However recognizing the space’s different strategies is important given different participants may be best served by one or the other. As tokenization continues to be adopted it’ll increasingly show which of these models best balances control, compliance, composability, access to liquidity, and scale.

Securitize

Focus: Equities, registered and private funds, and institutional DeFi

Total Value Tokenized: $3.3B (at the time of writing)

Overview:

Securitize is one of the most established tokenization platforms and the largest with $3.3B in tokenized assets, powering institutional issuances as their operating layer. Their biggest validation came in 2024 when they brought the world’s largest asset manager, BlackRock, onchain through their BUIDL token and Securitize has focused on regulated, large funds since then rather than generic token launches. Focusing on these kinds of assets makes it easier to build with their needs in mind such as fund administration, custody, and other factors that allow other large funds to also adopt. That being said, the trade-off is that priorities lie in regulated distribution, control, and permissions rather than permissionless DeFi access and movement. Nonetheless, the Securitize team builds with DeFi in mind and therefore has created their own standards and processes with partners in the space. Notable examples include their sToken standard which powered DeFi looping on Morpho and Kamino, expanding to multiple other DeFi platforms including UniswapX and Euler, co-creating the Trusted Single Source Oracle with RedStone for verifiable private fund NAV data onchain, and most recently Securitize shared their Vault Registrar for ownership attribution.

Securitize’s main focus in recent years has revolved around servicing institutional funds however they’ve recently returned to one of their original asset classes, equities, approaching them from a native tokenization perspective rather than the mirror token model. They are solving for tokenized stock prices through a hybrid approach, executing at the National Best Bid and Offer (NBBO) during trading hours and swiftly switching to AMM-style pricing after the closing bell for continuous secondary market availability.

KAIO

Focus: Tokenized funds, structured products, DeFi mobility and composability

Total Value Tokenized: $500M+ in cumulative transaction volume (at the time of writing)

Overview: Based in London and Abu Dhabi, with global operations, KAIO (formerly Libre) provides tokenization infrastructure for bringing institutional-grade investment funds onchain, covering issuance, compliance, distribution, and lifecycle management. The platform works with leading asset managers including BlackRock, Hamilton Lane, Laser Digital, Brevan Howard, and Mubadala Capital, enabling access to high-quality alternative investments through regulated structures.

KAIO focuses on compliant access rails for investors such as onchain treasuries, hedge funds managing liquidity onchain, or foundations as examples. Moving beyond onchain access and token management, KAIO’s modular design is also meant to add utility and composability to these assets in DeFi. They’re leading by example through their upcoming KASH token, a structured product meant to have stable yield from non-crypto-correlated assets such as the money market, private credit, and market neutral strategies. The KAIO Gateway allows dApps, distribution partners, liquidity providers, and other stakeholders to access tokenized assets on multiple chains and facilitates their utility while maintaining safeguards and compliance in place.

Centrifuge

Focus: Tokenized funds and DeFi

Total Value Tokenized: $1.5B (at the time of writing)

Overview:

Centrifuge is building infrastructure meant for institutional asset management, compliant issuance, and DeFi composability with protocol-level design choices being paramount. Their technology serves as underlying, standardized infrastructure issuers can build on themselves with a more white-glove service available through their Anemoy onchain asset management arm. Today this powers funds and their DeFi usage, giving investors tokenised access to assets and strategies managed/sub-managed by names such as Janus Henderson, Apollo, and S&P. A key architectural feature is native support for multiple share classes per pool, each with its own ERC-20 token, independent pricing, compliance hooks, and vault set, enabling traditional fund structures like Senior/Junior tranches or multi-currency classes directly at the protocol level. Centrifuge references ERC-20 share tokens, ERC-4626 for vault synchronous flows, ERC-7540 for asynchronous, and ERC-7575 for pooled vault structures in their documentation. As a result of building with these standards in place, issuers are able to build with templated workflows and the products they build are DeFi-ready for lending, liquidity, and portfolio management through their deRWA tokens. This becomes a more complex architecture compared to simple permissioned environments and therefore is best suited for managers truly looking for composability rather than mere digitization of their capitalization tables for operational efficiency.

A distinctive feature of Centrifuge’s protocol is full double-entry bookkeeping on-chain. Every pool maintains a complete general ledger with typed accounts (Asset, Equity, Gain, Loss, Expense, Liability), and all state changes — deposits, redemptions, NAV updates, holding revaluations — are recorded as balanced journal entries enforced at the smart contract level. This gives asset managers and auditors a transparent, verifiable accounting trail directly on-chain, rather than relying on off-chain reconciliation against blockchain state. No other tokenisation platform listed in this report offers comparable on-chain fund accounting.

WisdomTree

Focus: Tokenized funds and ETPs

Total Value Tokenized: $813M (at the time of writing)

Overview:

WisdomTree is a traditional asset manager that took it upon themselves to build their own apps for both retail and institutional clients alike. Largely led by their money market fund ($776M AUM), the ETF provider has launched 15 tokenized ‘40 Act funds available on 8 blockchains spanning exposures to treasuries, credit, and equities available on WisdomTree Prime (retail app) and WisdomTree Connect (institutional platform) in addition to other offerings including spot crypto and gold token offerings within the app. This company is internalizing a lot of the distribution and UI/UX rather than outsourcing, giving them more control over investor experience, subscription/redemption flows, and how the tokens are used. This makes sense for such a regulated player in the space and that control has become increasingly evident as the platform expands onramp/offramp options including partnering with BNY for their Banking-as-a-Service offering and enabling self-custody through whitelisted wallets registered to each holder. WisdomTree has also built knowing their audience best and for WisdomTree Prime that meant showing them how RWAs can be used in real life through their MMF-linked debit card, which redeems WTGXX tokens at the point of sale allowing users to earn yield until they use their assets rather than holding cash. That said, the control that comes with manager-specific platforms also presents trade-offs such as fragmentation rather than using a more shared infrastructure.

Nonetheless, compliance and control are justifiably a top priority and the forward-thinking asset manager is consistently solving for friction points, now supporting stablecoin subscriptions, continuous dividend accrual, and most recently their affiliated broker-dealer will support 24/7 money market fund redemptions for WTGXX at 1 USDC rather than redeeming with the fund once a day at NAV. One could expect the next evolution of the WisdomTree environment to entail DeFi integrations (likely embedded within the apps) for increased utilization of their tokenized assets – what could mean collateralized borrowing for a retail user on Prime could mean posting margin on Connect.

Superstate

Focus: Tokenized funds and public equities

Total Value Tokenized: $1B+ (at the time of writing)

Overview:

Beyond its role as a digital asset manager, Superstate is increasingly positioned as a technology provider, leveraging its institutional-grade infrastructure to support both proprietary funds and third-party managers through a unified tokenization platform. Their beginning focus was around fund tokenization, most notably their money market fund,USTB, and crypto carry fund, USCC, and the platform has since then extended to support native equity tokenization. Superstate’s implementation is especially interesting because it uses a hybrid fund-record architecture. Shares can be represented either as tokens or in book-entry form, and subscriptions or redemptions can be supported through both fiat and USDC rails. The benefit is that this reduces the leap required for traditional allocators, since it preserves familiar operational pathways while still enabling onchain transferability between allowlisted wallets and DeFi utility. Regarding native tokenization of shares, Superstate issues shares directly onchain rather than mirroring off-chain records. Through its SEC-registered transfer agent, investors can either subscribe to new issuances or migrate existing holdings into a tokenized format; these tokens represent the legal shares themselves. This model is designed to be easier to operationalize at scale while maintaining a bridge to traditional market infrastructure.

Ondo

Focus: Tokenized treasuries and public equities

Total Value Tokenized: ~$2.6B (at the time of writing)

Overview: Ondo Finance has become the largest provider of both tokenized treasuries and tokenized stocks, crossing $2.5B in TVL by January 2026 across two meaningfully different product lines serving meaningfully different investor types. Their fixed income suite starts with OUSG, a tokenized short-duration U.S. Treasury fund that holds primarily BlackRock’s BUIDL as its underlying vehicle and is available to qualified purchasers with 24/7 mint and redemption. USDY sits alongside it as a permissionless, yield-bearing token targeted at global non-U.S. investors, backed by Treasuries and bank demand deposits and designed to circulate freely across DeFi as a stablecoin alternative that actually pays yield. USDY crossed $1B in TVL on its own in early 2026 and is live on nine blockchains, reflecting real distribution breadth.

The more consequential launch has been Ondo Global Markets, which opened in September 2025 and brought tokenized U.S. stocks and ETFs to non-U.S. investors, with now over 260 names available via a mint-and-redeem model backed by Alpaca as the regulated U.S. broker-dealer. The platform became the largest tokenized equities venue by TVL within 48 hours of launch, and now has over $650M in TVL with over $12B in cumulative trading volume, capturing roughly 60% of that market. The tokens are designed to behave more like stablecoins than traditional security tokens: freely transferable, composable across DeFi, and accepted as collateral. In February 2026, Ondo expanded further with Global Listing for day-one IPO tokenization. Additionally, Ondo Perps for perpetual futures on tokenized equities is launching soon.

The regulatory picture is worth attention. The SEC formally closed its two-year investigation into Ondo in November 2025 without charges, and Ondo Global Markets subsequently made a confidential SEC registration filing, potentially making it the first issuer of transferable tokenized equities under SEC reporting requirements. On the infrastructure side, Ondo operates a full licensed stack, including an SEC-registered transfer agent, broker-dealer via the acquired Oasis Pro Markets, investment adviser, and ATS. The founding team comes from Goldman Sachs’ digital assets group and the platform has added former SEC and Treasury staff to its leadership.

Figure

Focus: Blockchain-native capital markets across multiple verticals

Total Value Tokenized: $21B+ in loans originated onchain (at the time of writing)

Overview: Figure is the most vertically integrated player in this space and operates at a scale that sets it apart from the platforms around it. Rather than starting with token design and working toward institutional adoption, Figure built from the lending side: originating home equity lines of credit on the Provenance Blockchain since 2018, and progressively moving up the capital markets stack until it owned the full pipeline from origination through securitization and trading. With over $21B in loans originated onchain and more than $50B in total blockchain transactions, Provenance is the highest-volume public blockchain for tokenized real-world financial assets.

The commercial validation is genuinely notable. Figure’s most recent securitization received AAA ratings from both S&P and Moody’s, the first for any blockchain-native securitization, which matters because it demonstrates that traditional credit rating infrastructure is now willing to assess and underwrite onchain structures at the top of the scale. The company listed on Nasdaq in September 2025 as FIGR, reporting 2025 full-year revenue of $507M and net income of $134M. That makes it one of the very few profitable, publicly traded pure-play blockchain finance companies in existence. Consumer Loan Marketplace Volume reached $816M in January 2026 alone, up 115% year-over-year.

The product suite continues to broaden. $YLDS is the first SEC-registered, yield-bearing stablecoin, with $376M in circulation as of January 2026 and growing at 15% monthly. Democratized Prime is Figure’s onchain lend-borrow marketplace, positioning itself as a blockchain-native prime brokerage alternative for tokenized asset holders, with $253M in matched offers in January 2026. The most ambitious move was OPEN, the onchain Public Equity Network launched in January 2026, which allows companies to list their equity directly as blockchain-registered securities rather than as tokenized wrappers of existing DTCC instruments. OPEN equities trade on Figure’s own ATS limit order book, with BitGo providing custody and Jump Trading signed on as market maker. Figure itself filed to be the first issuer. For anyone studying what a fully blockchain-native capital market stack looks like at institutional scale, Figure is the reference case.

Tokeny (acquired by Apex)

Focus: Enterprise tokenization infrastructure and compliance standards

Total Value Tokenized: $32B+ facilitated through ERC-3643 infrastructure (at the time of writing)

Overview: Tokeny sits in a different part of the stack from most platforms in this report. Rather than issuing its own tokenized products, it provides the operational and compliance infrastructure that other institutions use to do so, making it closer in nature to a transfer agent or technology provider than an asset manager or protocol. The $32B figure represents total assets tokenized by its clients using its platform, not proprietary AUM, which is a meaningful distinction but also a testament to how widely its technology has been adopted.

The company’s defining contribution to the space has been the creation and open-sourcing of ERC-3643, the most widely adopted token standard for compliant security tokens. Built on top of ERC-20 with an embedded compliance layer, ERC-3643 links token ownership to verifiable onchain identities through the ONCHAINID protocol, allowing issuers to enforce investor eligibility, transfer restrictions, and jurisdiction-based controls directly at the smart contract level while remaining interoperable with the broader EVM ecosystem. When a transfer is initiated, the token verifies the sender and receiver’s ONCHAINID status in real time against predefined compliance rules before executing. Crucially, Tokeny open-sourced the standard rather than keeping it proprietary, which is what gave it the reach it now has. The ERC3643 Association has grown to 78 institutional members including DTCC, Fireblocks, Deloitte, Chainlink Labs, Ava Labs, and OpenZeppelin.

In May 2025, Apex Group, a fund services provider with $3.5T in assets under administration across 52 countries, acquired a majority stake in Tokeny and folded it into Apex Digital 3.0, its institutional tokenization offering. This changes Tokeny’s trajectory substantially: where its technology reach was previously limited by its own distribution capacity, it now plugs into Apex’s existing relationships with asset managers, custodians, and fund administrators globally. Recent work includes the tokenization of SkyBridge Capital’s $300M hedge fund and a partnership with AMINA Bank to combine Swiss banking-grade custody with Tokeny’s issuance layer. For asset managers evaluating tokenization infrastructure, Tokeny sits upstream from most of the platforms in this report. It is the compliance and standards layer that many of them, or their competitors, will need to build on.

Spiko

Focus: Tokenized UCITS money market funds for corporate cash management

Total Value Tokenized: ~$1.2B (at the time of writing)

Overview: Spiko is a Paris-based fintech that has taken the most regulation-forward path in the European tokenization market. Founded in 2023 by former French Treasury officials with backgrounds at Palantir, the company launched what are recognized as the first UCITS-compliant money market funds with a fully tokenized share registry on public blockchains — meaning the blockchain is the legal register of record rather than a digital copy of an off-chain one. UCITS is the EU’s most widely recognized and distributed fund framework, which gives Spiko’s products access to a significantly broader investor base than most tokenized fund structures that rely on Reg D exemptions or jurisdiction-specific carve-outs — a reach reflected in EUTBL becoming the largest euro-denominated tokenized cash equivalent, ahead of euro-denominated stablecoins.

The three core funds are USTBL, investing in the U.S. T-Bills, EUTBL, investing in French and Eurozone government Treasury Bills, and UKTBL, investing in UK Treasury Bills. All three are regulated by France’s AMF, audited by PwC, and use CACEIS (a Crédit Agricole subsidiary) as the custodian bank, with Twenty First Capital as investment manager. Spiko acts as its own transfer agent onchain, eliminating the traditional fund administration intermediary and passing the efficiency gains through in the form of a simple 0.25% annual management fee with no deposit, withdrawal, or currency conversion fees. Shares accrue daily interest at the risk-free rate and can be subscribed using either fiat or stablecoin, with cross-currency orders using Bloomberg BFIX rates so a euro-based client can invest in the USD or GBP funds without incurring conversion costs.

On DeFi composability, Spiko has integrated Chainlink’s CCIP to allow cross-chain transfers of fund shares across Ethereum, Arbitrum, Polygon, Starknet, and Etherlink without investors needing to redeem and resubscribe between networks. Spiko also partnered with SG-Forge in September 2025 to give fund shareholders 24/7 access to stablecoin liquidity through Morpho. In July 2025, the company raised a $22M Series A led by Index Ventures, with Revolut co-founder Nikolay Storonsky, Blackstone co-CIO Lionel Assant, and Bridge co-founder Zach Abrams among the angels. In February 2026, 18 months after launch, Spiko crossed $1B in AUM across four products and over 3,300 active clients, placing it alongside BlackRock, Franklin Templeton, and Fidelity in tokenized fund scale. The platform’s B2B distribution approach, targeting European corporate treasuries sitting on idle cash via API integrations with fintech partners, is a more grounded growth strategy than most crypto-native platforms have attempted.

Theo

Focus: Full-stack tokenization with integrated market-making, liquidity, and DeFi composability Total Value Tokenized: ~$200M+ in thBILL TVL (at the time of writing)

Overview: Theo’s organizing thesis, which it calls “beyond issuance,” starts from a specific observation about why tokenized asset markets underperform: most platforms solve for token creation but leave distribution and trading to chance. The result is institutionally backed products that technically work but see little to no secondary activity. Theo’s answer is to bundle continuous market-making, cross-chain liquidity, and DeFi integration into the platform itself, treating liquidity as a product feature rather than something issuers have to source on their own. The founding team comes from Optiver and IMC Trading, two of the highest-volume market-making firms in traditional finance, and $20M in Series A funding came from Hack VC, Mirana Ventures, and Anthos Capital, with traders from Citadel and Jane Street as angels.

The flagship product, thBILL, is structured as an index of institutional-grade tokenized Treasury products rather than a standalone fund. It aggregates underlying exposure through tULTRA, a token-native fixed income fund managed by Wellington Management via FundBridge Capital and enabled by Libeara, the tokenization platform backed by Standard Chartered Ventures. Theo then wraps that institutional-grade backing with its own continuous market-making and distribution infrastructure, with liquidity provided by SIG, Flowdesk, and Amber. The result: $200M+ in TVL and $1B in cumulative trading volume within four months of launch, with 15 DeFi integrations and 80,000+ users across 60 countries. The token uses ERC-4626 for seamless DeFi composability and is live on Ethereum, Arbitrum, Base, and HyperEVM.

In January 2026, Theo launched thGOLD, a yield-bearing tokenized gold product that earns approximately 2.3% net annual yield by lending physical gold to established retailers through FundBridge’s MG999 onchain Gold Fund, a structure that goes meaningfully beyond the simple spot-price wrappers that dominate the tokenized gold market. thGOLD is tradeable and usable as collateral across Hyperliquid, Uniswap, Morpho, and Pendle. Most recently, Theo announced thUSD, a stablecoin built on a delta-neutral gold carry strategy that simultaneously holds thGOLD and shorts gold futures on the CME, capturing both the gold lending yield and the futures basis spread as a structural yield source. The progression from a tokenized Treasury basket to yield-bearing gold to a delta-neutral stablecoin reveals a team iterating toward increasingly sophisticated product structures, each time using the same institutional partner stack and market-making infrastructure. For a platform less than two years old, the trading velocity and product breadth are among the more credible signals in the space.

What’s Next: Into Part 2

The first half of this report has been about architecture: where compliance logic lives, how identity gets represented onchain, and why the design choices made at the token layer ripple through everything that follows. The four operating models covered here are not just strategic preferences, they are bets on where the market’s center of gravity will settle.

But none of that infrastructure matters unless the assets it produces actually get used. Part 2 shifts the question from how tokenized assets are issued and controlled to how they become economically active. That means vaults, the structures that turn a tokenized RWA from a held position into productive collateral for lending, yield strategies, and portfolio management. It is also where the compliance and custody decisions from Part 1 start having real consequences in practice. An asset that cannot be posted as collateral, looped, or integrated into a DeFi strategy has limited utility beyond digitizing a cap table.

Part 2 covers the vault standards enabling this, the curator and allocator behavior emerging on platforms like Morpho and Aave, and what the early data reveals about how institutional capital is actually moving onchain.

Get access to the second part of the report.

Sign up to unlock the full report link, delivered straight to your inbox.

Get access