Key Takeaways

- Traditional finance has spent a century building yield infrastructure. Crypto hasn’t caught up just yet. Yield-generating assets make up just 8-11% of crypto markets versus 55-65% of TradFi. That’s a 5-6x development gap, but yield bearing assets are positioned for significant growth as the “Crypto-as-Infrastructure” thesis gains traction.

- The GENIUS Act is being called the most significant catalyst for crypto since the Bitcoin whitepaper. The timing couldn’t be better. As clarity emerges, yield bearing stablecoins are exploding: market capitalization is up 300% YoY, with new protocols launching monthly to capture the opportunity.

- Blue-chip yield products are gaining major momentum. ETH liquid staking tokens (LSTs) surged from 6 million to 16 million between 2023 and November 2025, adding $34 billion in notional value at current prices. SOL LSTs doubled over the same period, adding $10 billion in market cap. Meanwhile, Bitcoin yield products are emerging as the next frontier.

- Yield bearing Real-World Assets (RWAs) are bridging TradFi and onchain finance. Traditional institutions recognize the efficiency gains and are accelerating tokenization efforts. Beyond stablecoins, Private Credit and US Treasuries are leading the charge, capturing the largest capital inflows across all tokenized asset categories.

- DeFi runs on yield bearing assets (YBAs). ETH and SOL LSTs alone account for roughly 30% of TVL in AAVE and Kamino. The relationship is symbiotic: new YBAs gain instant distribution through integrations with major DeFi protocols like AAVE, Morpho, Euler, and Pendle, while these platforms deepen their liquidity and network effects. This composability is what separates crypto yield from TradFi: returns can be stacked, leveraged, and amplified across protocols.

- Infrastructure will separate winners from noise. As YBAs scale toward a trillion-dollar market, institutional adoption hinges on robust curation, risk assessment, and resiliant oracle frameworks. This is where Credora‘s standardized risk evaluation for assets and DeFi strategies, combined with RedStone‘s secure and scalable oracle infrastructure, becomes critical. The protocols that select reliable partners and carefully operate on the risk vs yield relationship today will define onchain finance tomorrow.

Featured Projects and Organizations

Contributors

RedStone, as the main author of the report, would like to express true gratitude to all the contributors, projects, and key opinion leaders who helped us create such a comprehensive piece on the yield bearing assets landscape. Starting with big gratitude towards Gauntlet, Stablewatch Tokenized Asset Coalition and DL Research teams, especially the research department, for their diligent and timely work. The depth and breadth of this report wouldn’t be possible without these individuals. Special thanks to Johnny from TAC, Max and Kabal from Stablewatch, Simon, Jake, and Delz from Gauntlet, Sebastian from DL Research and multiple other kind contributors to the final report.

| Yield Bearing Digital Assets Overview | ||||||

| Synthetic Stablecoins | Liquid Staking Tokens | Liquid Restaking Tokens | Yield on Bitcoin | Tokenized RWA | Tokenization Platforms for Yield assets | Yield Protocols |

| Ethena (USDe & sUSDe) | Lido (wstETH) | EtherFi (weETH) | Lombard (LBTC) | BlackRock (BUIDL, CASH) | Securitize | Spark |

| Spark (sUSDS) | Rocketpool (rETH) | Renzo (ezETH) | YieldBasis | VanEck (VBILL) | KAIO | Morpho |

| Gautlet (gtUSDa) | Kinetiq (kHYPE & iHYPE & vHYPE) | Puffer (pufETH) | Syntetika | Franklin Templeton (BENJI) | Centrifuge | Euler |

| Axis (xyUSD) | stakedhype (stHYPE) | Kelp (rsETH) | Maple Finance | Superstate (USTB) | Spiko | Aave |

| Maple (syrupUSDC) | Hyperbeat (beHYPE) | Jito (jitoSOL) | Apollo (ACRED) | Tradable | Kamino | |

| Resolv (stUSR, RLP) | Jupiter (jupSOL) | Hamilton Lane (SCOPE) | Wisdomtree | Pendle | ||

| AAVE (GHO) | Marinade (mSOL) | Janus Henderson (JTRSY) | Ondo | OpenTrade | ||

| Native Markets (USDH) | Laser Digital (CARRY) | Superstate | ||||

| Almanak (alUSD) | Brevan Howard (MACRO) | Midas | ||||

| Upshift (CoreUSD) | Invesco(iSNR) | DigiFt | ||||

| UBS (uMINT) | Libeara | |||||

| Wellington Management (ULTRA) | Theo | |||||

| Fidelity (FDIT) | OpenEden | |||||

| Ondo (OUSG & USDY) | Paxos | |||||

| Hadron Tether | ||||||

| Archax | ||||||

| PACT | ||||||

| Tokeny | ||||||

| Brickken | ||||||

Join The Low-Risk DeFi Movement,

Online and at Devconnect Argentina

Yield Rules Everything. Crypto YBAs Are Next.

Traditional finance runs on yield. Pension funds, insurance companies, sovereign wealth funds, banks: the entire machinery of global capital allocation depends on predictable income streams. Retirees receive monthly checks because their savings generated returns over decades. Corporate treasuries fund operations by parking cash in yield-generating vehicles. National fiscal planning assumes government bonds will pay interest reliably.

The numbers reflect this reality. Global financial markets reached $247 trillion across major asset classes by January 2025, according to Ocorian’s Global Asset Monitor. Yield-generating instruments dominate: bonds ($141 trillion), dividend-paying equities (estimated $50-60 trillion), and REITs ($2 trillion) collectively represent 55-65% of investable capital. More than 100x larger than crypto, traditional finance has built itself around interest-bearing assets.

Yield bearing assets are the bedrock of global finance.

Crypto presents a stark contrast. With a total market capitalization of $3.55 trillion (source: CoinGecko, November 2025), only $300-400 billion generates yield. That’s just 8-11% of the asset class.

The breakdown includes staked assets ($130B in ETH, $66B in SOL, $28B in BNB, plus ~$10B in others, source: Token Terminal, Staking Rewards, November 2025), yield bearing stablecoins ($22B, source: stablewatch, November 2025), and DeFi deposits ($116B total: $22B in DEXs, $94B in lending protocols, source: Artemis, November 2025). The contrast is even starker than it appears. This 8-11% yield rate is likely inflated due to double-counting between overlapping categories. For instance, wstETH deposited into Aave adds up to the both staking and DeFi metrics.

The gap is striking: traditional finance has structured itself around yield generation for over a century, while crypto remains an overwhelmingly appreciation-driven market. In percentage point terms, the disparity is clear. Yield-generating assets comprise just 8-11% of crypto, compared to 55-65% of traditional finance, making crypto’s yield infrastructure 5-6x underdeveloped relative to TradFi.

But this gap represents crypto’s greatest opportunity. As the “Crypto-as-infrastructure” thesis gains traction and onchain finance proves its superior capital efficiency, yield-generating crypto assets are positioned for exponential growth. Institutional capital follows efficiency. Clear regulation across major jurisdictions removes the final barrier.

Crypto Yield Bearing Assets (YBAs) are positioned for exponential growth in months to come as the “Crypto-as-Infrastructure” thesis gains traction.

But here’s where crypto’s story gets even more interesting. For institutions, yield bearing crypto assets became relevant only recently, and understanding why requires looking at what changed. Back in 2020 and earlier, blue-chip crypto assets had extreme volatility: 100%+ annualized swings. In that environment, earning 4-8% yield on top didn’t move the needle. The institutions in crypto back then understood this. But most of today’s institutional capital wasn’t in the space then. They missed the wild volatility era entirely.

Two things shifted in parallel. First, crypto blue-chips like Bitcoin, Ethereum, and Solana matured significantly. ETF approvals, regulatory clarity, and institutional custody infrastructure transformed these from speculative bets into allocatable assets. Valuation frameworks emerged more broadly for quantifying L1 cryptocurrencies, giving analysts tools to model these assets beyond pure price speculation. Second, and perhaps more importantly, DeFi evolved beyond pure crypto assets. Massive growth in stablecoin usage and RWA tokenization gave traditional finance institutions their revelation: onchain finance, specifically DeFi infrastructure, offers fundamentally superior capital efficiency compared to legacy rails.

The breakthrough isn’t just crypto maturing as an asset class. It’s crypto revealing itself as the underlying infrastructure that delivers exponentially better capital efficiency for trillions of dollars worth of assets. Stablecoins deployed into money markets generate continuous yield with block-by-block interest settlement, treating time as a continuous function rather than the fixed terms of traditional finance. Tokenized traditional assets can produce higher yields while being plugged into DeFi infrastructure, gaining access to deep secondary liquidity built atop battle-tested protocols. Bitcoin, Ethereum, and other blue-chip assets generate yields through DeFi protocols that can rebalance across multiple primitives. Years of iteration on top of now-legacy DeFi infrastructure have sharpened these strategies, driving risk-adjusted capital efficiency to unprecedented levels. Emerging platforms like Hyperliquid push efficiency further. Staking rewards, lending interest, RWA yields, protocol mechanisms: capital working harder than legacy infrastructure allows. This is cold, hard economics. The onchain rails simply make more financial sense for managing assets, whether crypto-native or tokenized tradfi ones.

Institutions follow efficiency, and onchain finance provides exactly that.

The barrier to institutional adoption at scale is risk transparency. Technical and economic risks vary wildly, even within the same asset categories. A stablecoin backed by US Treasuries carries different risks than one relying on algorithmic mechanisms. A liquid staking protocol operated by established validators isn’t comparable to one run by new entrants. However, distilling these insights isn’t straightforward for institutions accustomed to relying on established rating agencies for risk evaluation in traditional finance. Without comparable standardized frameworks in crypto, most institutional players lack the tools to evaluate onchain risk independently. Yield opportunities exist, but risk transparency doesn’t. Buying blind isn’t due diligence.

Credora by RedStone provides standardized risk evaluation that brings institutional-grade analysis to crypto-native assets.

Throughout this report, Credora’s asset rating spotlights dissect what drives each asset or strategy’s risk and return profile. This isn’t about constraining innovation. It’s about giving crypto the transparency infrastructure that matches its capital efficiency advantage, serving common investors, crypto degens, and institutions alike.

By builders, for builders.

Throughout this report: Asset Spotlights featuring Credora ratings highlighting the key factors driving each asset.

Note: All data sources are listed in the References section.

The Rise of Yield Bearing Stablecoins

The GENIUS Act is the most important event for this industry since the Bitcoin whitepaper.

That’s what many industry experts are saying today. And by all means, it shows. Every financial participant is positioning for stablecoins to be the next trillion-dollar opportunity. Central banks, commercial banks, brokerages, traditional institutions, and crypto-native players are all moving fast. With this explosion of interest, attention has naturally shifted to yield bearing stablecoins (YBS). The yield component is a key value proposition for projects trying to break the Tether and Circle duopoly. But there’s much more to it than meets the eye. That’s what Stablewatch, the report’s co-author, is here to spotlight in their YBS landscape overview.

Get the full YBS overview by visiting the link below.

Read the Yield Bearing Stablecoin Landscape Report

By Stablewatch

Evaluating risk factors for stablecoins is extremely important, and here’s a taste of what Credora ratings will be built upon. We’re taking a closer look at the yield bearing version of USDS, the stablecoin issued by Sky Protocol (formerly MakerDAO). Sky backs USDS with a mix of tokenized treasuries and crypto-native collateral, publishes fully transparent reserve composition with real-time reporting, and maintains a comprehensive $10m bug bounty program. With DAI’s 6+ year track record and widespread DeFi integration, USDS represents one of the most battle-tested stablecoin infrastructures in crypto.

Yield Bearing Blue-Chips: Crypto Yield Is Real

Blue-chip crypto assets like BTC, ETH, and SOL no longer just sit idle. They generate yield. And the market has responded by treating yield bearing versions as the new default format for holding value onchain.

This shift from passive holdings to productive capital isn’t speculative. It’s structural. ETH is held as stETH or eETH. SOL moves into JitoSOL or jupSOL. Bitcoin, long resistant to any form of native yield, now has protocols like Babylon enabling staking functionality. The crypto market is following a path finance has taken for centuries: capital that generates a return outcompetes capital that doesn’t.

The Rise of YBAs – From Preference to Standard

The shift towards productive capital in crypto is now reshaping how liquidity enters, moves, and settles across the ecosystem. Over the past few years, yield bearing assets have progressed from being an optional strategy to becoming the default format for holding value onchain.

This is visible in user behaviour, liquidity composition, and institutional flows. Where participants once held base assets, they now increasingly hold productive formats:

- ETH is held as stETH, eETH, ETHx, and other LSTs and LRTs

- SOL migrates into liquid staking formats such as mSOL, JitoSOL, and jupSOL

The result is straightforward: idle capital is becoming the exception, not the norm.

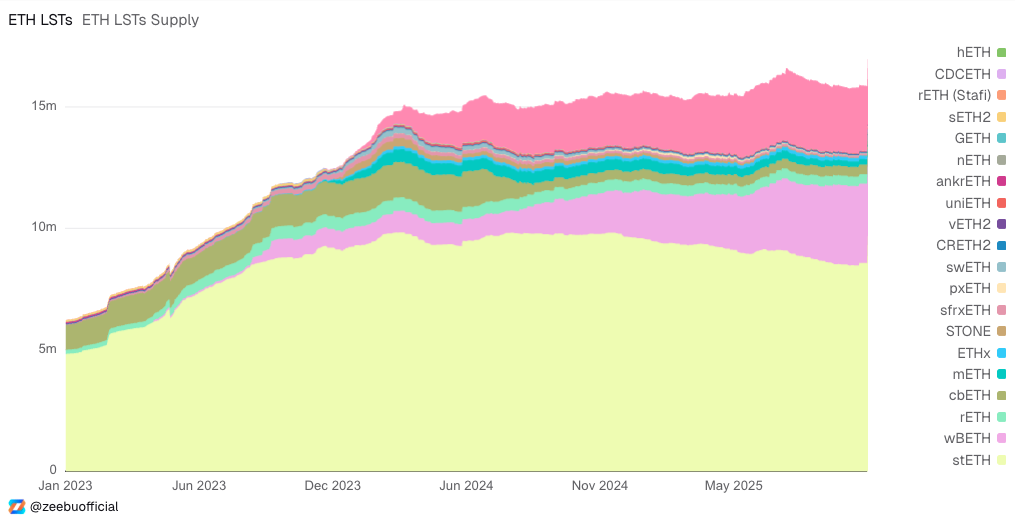

Market data supports this structural change. Liquid-staked ETH has increased from roughly six million ETH in early 2023 to more than sixteen million today, representing approximately 12% of circulating supply and around 40% of all staked ETH (around 30% of ETH is currently staked).

Solana shows the same trajectory. Liquid-staked supply has nearly doubled from roughly 20 million SOL to over 40 million since January 2024. Approximately 67 percent of SOL is now staked, and liquid staking represents about 8 percent of total supply, led by Jito, Marinade, and Jupiter, with Binance’s recent entry further accelerating adoption.

The Layers of Blue-Chip Yield

Yield bearing crypto assets come in layers of increasing complexity, each building on what came before.

Liquid Staking Tokens (LSTs) solved a basic problem: staking locks up capital. LSTs like Lido’s stETH or Rocketpool’s rETH let holders stake ETH and receive a liquid token in return, maintaining exposure to staking rewards while keeping assets usable in DeFi.

Liquid Restaking Tokens (LRTs) added another layer. Protocols like Ether.fi’s eETH, Renzo’s ezETH and Kelp’s rsETH (using EigenCloud restaking infrastructure) allow staked ETH to secure additional networks and services beyond Ethereum itself, earning multiple yield streams. The same collateral underwrites multiple protocols simultaneously, increasing capital efficiency.

The Hyperliquid ecosystem is experimenting with a hybrid approach that could resemble native restaking. Through HIP-3, LST providers like Kinetiq, stakedhype and Hyperbeat could leverage staked HYPE to build new perpetual markets while still validating consensus. Instead of just tokenizing staking receipts, these protocols would function more like capital allocators, offering delegators yield strategies that vary between providers. It’s still early and nowhere near the scale of Ethereum or Solana LSTs, but it hints at a potential next chapter: liquid staking that builds markets, not just validates them.

There is a lot of layered complexity within staking and restaking blue chip crypto tokens, and Credora will shed light on all of this. We’re examining eETH, the liquid restaking token issued by Ether.fi. eETH is backed 1:1 by ETH and stETH through a non-custodial architecture, with all staking and restaking positions recorded on-chain for real-time verification. As the leading liquid restaking protocol with $8.6b in TVL, Ether.fi has demonstrated strong secondary market liquidity, experiencing depeg events greater than 1% for only ~10 days in the past year.

Bitcoin’s Yield Renaissance

Bitcoin resisted yield for over a decade. Its design doesn’t include staking. Its culture prized immutability over composability. But that’s changing.

Babylon introduced Bitcoin staking by letting BTC secure proof-of-stake chains without wrapping or bridging assets. The BTC gets locked in a vault on Bitcoin’s own blockchain, using Bitcoin’s native scripting language. A cryptographic proof confirms the lock, allowing the staked BTC to validate blocks on PoS chains. If validators misbehave, the protocol exposes their private keys, enabling the locked Bitcoin to be slashed as penalty. The system uses Bitcoin’s proof-of-work blockchain as a security anchor, tying PoS chain checkpoints to Bitcoin’s finality.

Babylon Protocol now holds roughly $6 billion in TVL, close to 60,000 BTC. Extremely impressive for still a rather nascent protocol.

Babylon also enables liquid staking derivatives. Protocols like Lombard Finance and PumpBTC issue yield bearing tokens (LBTC and yBTC) backed by Babylon-staked BTC, functioning similarly to Lido’s stETH for Ethereum. These derivatives make Bitcoin yield usable in DeFi while maintaining exposure to BTC.

BTC derivatives such as wBTC and cbBTC have also found a role, generating yield opportunities across DeFi. Services like Maple Finance run BTC loan origination, allowing institutions to borrow against Bitcoin collateral. The model brings Bitcoin into structured credit markets, generating yield for lenders while keeping the underlying asset as BTC exposure.

Curve founder Michael Egorov’s new project, Yield Basis, is bringing yield to Bitcoin through automated market-making strategies that solve impermanent loss using leverage. Synthetika is drawing similar attention with their upcoming “Basis+” BTC strategy, shBTC.

Bitcoin holders want yield. The market is building infrastructure to deliver it.

Institutional Appetite and Risk Perception

Traditional finance investors remain cautious about crypto-native blue-chip assets. For most institutions, Bitcoin already sits at the tail end of their risk curve. Moving further into ETH or SOL requires a risk appetite that institutional mandates often don’t allow.

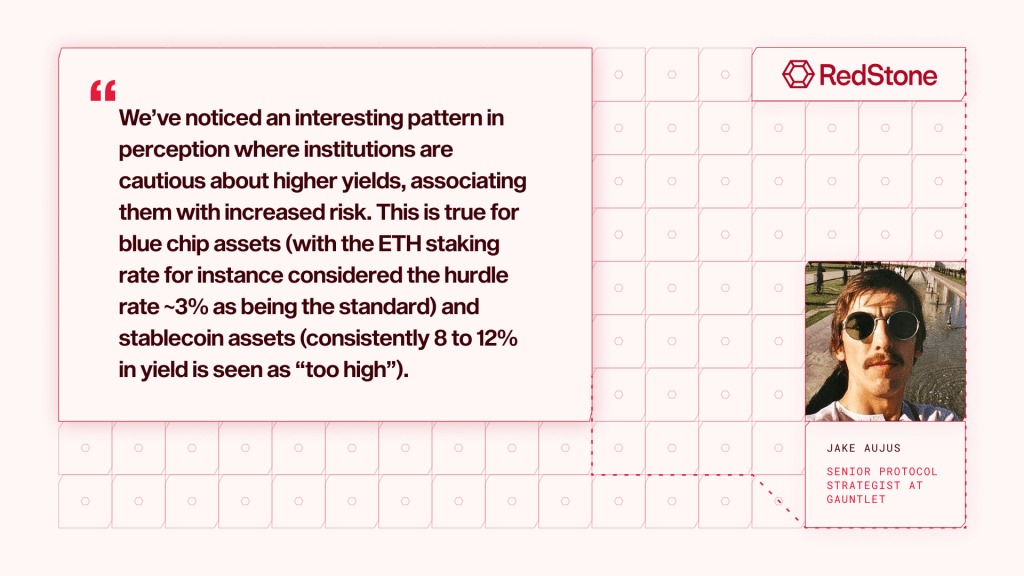

Gauntlet, a leading risk management platform in DeFi, observes that LSTs, LRTs, and BTC yield derivatives respond to a market need for institutions seeking exposure to underlying assets while generating yield above hurdle rates. But these strategies remain a small fraction of institutional crypto activity. Institutions favor stablecoin-based yield strategies over volatile asset strategies. The complexity matters. Yield strategies on blue-chip crypto assets often involve borrowing in stablecoins and swapping into yield derivatives. That’s a multi-step process requiring active management and risk oversight. Stablecoin yield, by contrast, is direct and predictable.

Gauntlet also notes an interesting pattern in perception:

DeFi protocols offer yields that would be extraordinary in traditional finance, yet institutions remain skeptical precisely because those yields seem unsustainable. Where blue-chip yield strategies do find traction is with Digital Asset Treasury (DAT) companies. These entities hold crypto assets on their balance sheets and differentiate themselves through yield strategies. NASDAQ-listed DeFi Development Corp. ($DFDV), for example, holds Solana and deploys it through dfdvSOL, an LST that generates yield via an onchain strategy designed by Gauntlet on Drift. This approach maintains SOL exposure while earning returns.

As for whether blue-chip crypto assets will remain central to DeFi’s growth, Gauntlet suggests their percentage impact may diminish if DeFi moves into the underlying rails of traditional finance rather than remaining a parallel ecosystem. As stablecoins and tokenized real-world assets grow, DeFi could shift from being a crypto-native playground to becoming infrastructure for traditional finance. In that scenario, BTC, ETH, and SOL might become less central to DeFi activity.

But that’s a long-term question. For now, blue-chip crypto assets remain the foundation of onchain liquidity. They’re the collateral that backs lending protocols, the assets that seed liquidity pools, and the yield-generating primitives that attract both retail and institutional capital.

The ETF Effect

Bitcoin, Ethereum and recent Solana ETFs have brought billions into crypto without requiring investors to hold assets onchain. That changes the blue-chip landscape.

ETFs pull liquidity out of DeFi. Why stake ETH onchain when you can hold an ETF in a brokerage account with no gas fees, no wallet management, and familiar regulatory protections? The convenience is significant, and for many institutions, it outweighs the yield opportunity.

But yield bearing ETFs could reverse this dynamic. If regulators approve staking ETFs, institutions could capture ETH staking rewards without ever interacting with DeFi directly. That would legitimize crypto yield for traditional investors, potentially unlocking capital that currently sits in non-yielding ETF products.

The irony is that yield bearing ETFs could validate DeFi’s model while routing capital away from DeFi protocols. Institutions would earn staking yield, but the actual staking would happen through custodians and ETF providers, not through direct protocol participation.

Real-World Assets: Yield Brings TradFi Onchain

The tokenization story started when nobody called it tokenization. Stablecoins emerged to solve a practical problem: crypto needed a stable, non-volatile unit of account. Trading against BTC’s wild price swings made little sense for everyday users. The industry needed something more intuitive, something that felt familiar. The answer was obvious. Bring the U.S. dollar onchain, the global standard everyone already understood and trusted.

What began as a simple utility became something far bigger. Stablecoins weren’t just convenient. They were the first real-world assets to prove that traditional value could live onchain. Today, they remain the most important RWA class by every metric that matters: capitalization, transaction volume, regulatory attention, and public awareness.

This dominance is impossible to ignore. Stablecoins represent 90% of all tokenized assets, with USDT commanding over $180 billion in supply compared to USDC’s $75 billion.

From stablecoins, the expansion into broader real-world assets feels inevitable. RWAs now span everything from physical gold and real estate to government bonds, loans, and IP royalties. These tokens represent actual claims: gold bullion sitting in vaults, dollars held in reserve accounts, ownership stakes in physical property. The blockchain component isn’t just digital record-keeping. It enables 24/7 trading, instant settlement, and composability with DeFi protocols in ways traditional finance infrastructure never could.

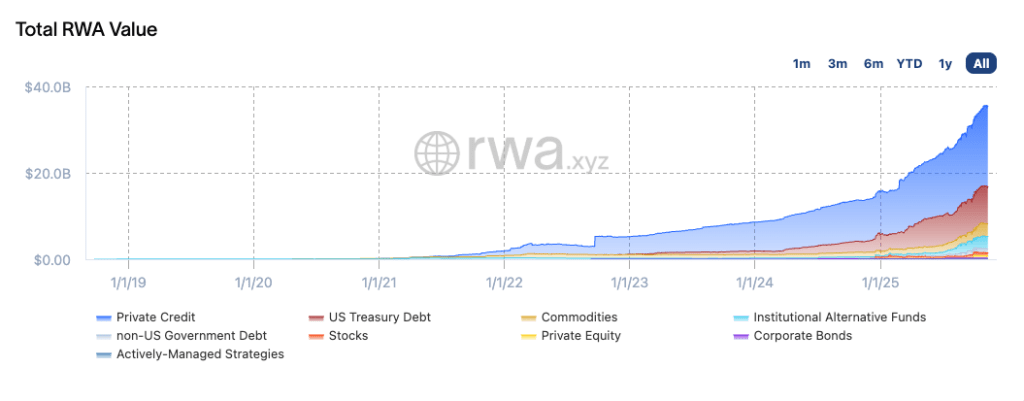

The real growth story of RWAs started by late 2022. Rising global interest rates made U.S. Treasuries attractive again after years of near-zero returns. Crypto investors wanted access to these yields without leaving the blockchain. Institutions that had watched from the sidelines for years were finally ready to experiment. Regulatory clarity improved. Major asset managers started tokenizing Treasury bill funds and private equity positions on both public and permissioned chains.

The market moved fast. Onchain RWA markets grew from roughly $5-10 billion in 2022 to over $36 billion by November 2025. The first half of 2025 alone saw the RWA market surge approximately 260%, jumping from $8.6 billion to over $23 billion.

BlackRock’s CEO, Larry Fink, declared that “the next generation for markets will be the tokenization of securities.” Consulting firms, financial institutions, and government agencies increasingly project that the tokenization industry will reach trillions by the end of the decade.

Source: RWA.xyz

Traditional finance is recognizing what blockchain delivers that previous digitization attempts couldn’t: global accessibility, real liquidity improvements, and dramatically reduced dependence on intermediaries.

Then came the GENIUS Act. This changes everything. Along with other U.S. crypto legislation now moving through Congress, GENIUS represents the regulatory unlock the industry has been waiting for. Banks, asset managers, and financial institutions can finally move forward with full confidence. The compliance frameworks are coming. The legal uncertainties that kept traditional players cautious are dissolving. What took years to build in terms of technology and infrastructure now has the regulatory foundation to scale exponentially.

This regulatory clarity is driving rapid growth in tokenization platforms.

Large institutions could build this infrastructure themselves, but the economics tell a different story. These are massive corporations where everything moves slowly, and most are years behind the blockchain technology curve. Building in-house means hiring specialized blockchain and DeFi experts in a niche industry where talent is scarce and expensive. It’s faster, cheaper, and frankly better quality to use platforms already deep in the technological trenches. Securitize, KAIO, Centrifuge, Spiko, Tradable, WisdomTree, Ondo, Superstate, Midas, DigiFt, Libeara, Theo, OpenEden, Paxos, Hadron by Tether, Archax, PACT, Tokeny, and Brickken are all competing to become the standard for issuing, managing, and distributing tokenized securities. The infrastructure buildout is happening now.

Why Bring TradFi Yields Onchain?

Traditional institutions aren’t moving onchain because of narratives or crypto enthusiasm. The decision is driven by hard economics: capital efficiency and cost reduction. Tokenization makes financial sense when it directly impacts the bottom line.

The math is straightforward. Blockchain infrastructure cuts administrative overhead through automated fund operations and compliance processes. Manual reconciliation, intermediary fees, and legacy system maintenance costs drop significantly. Settlement happens in real time instead of T+2 or longer, freeing up capital that would otherwise sit idle. Geographic barriers disappear, opening access to global liquidity pools that were previously out of reach.

Capital efficiency gains are even more compelling. Traditional finance operates with layers of intermediaries, each taking a cut and adding friction. Onchain systems reduce these layers dramatically. Assets can be borrowed against with far less friction. Collateral moves instantly across borders and platforms. But the real unlock goes beyond replicating traditional finance more efficiently. Tokenization enables strategies that are extremely difficult or impossible in TradFi.

Take underwriting a loan on a long-tail exotic asset. Try convincing a traditional finance manager to provide collateral against illiquid assets like shares in private credit markets. The friction is immense. In DeFi, battle-tested protocols proven by billions in settlement volume handle this programmatically. Smart contracts manage the entire collateral and leverage stack without manual intervention. Strategies that would be capital-constrained or operationally prohibitive in traditional finance become straightforward onchain.

Secondary market liquidity improves too, particularly for long-tail assets that lack established secondary trading infrastructure or market depth in traditional finance. Tokenized assets trade 24/7 on global platforms rather than being locked in settlement cycles. This technological step forward creates liquidity where none existed before. The challenges around redemption mechanics, continuous versus fixed-term financing, and risk management remain real considerations, but the infrastructure to address them is developing rapidly.

The appeal for DeFi-native participants flips the perspective entirely. These players seek yield uncorrelated with cryptocurrency markets, backed by real-world cash flows, accessible through permissionless infrastructure. They want diversification and alpha opportunities beyond volatile crypto assets. And the tailwind is demographic. Younger generations controlling more global capital are crypto-native and crypto-aware. They’re comfortable with onchain systems in ways older generations aren’t. This generational shift favors long-term capital movement into space. The convergence is happening because both sides gain something concrete.

The cambrian explosion of yield bearing RWA products makes this clear: BlackRock’s BUIDL, VanEck’s VBILL, Franklin Templeton’s BENJI, Apollo’s ACRED, Hamilton Lane’s SCOPE, Janus Henderson’s JTRSY, Brevan Howard’s Master Fund, Invesco’s iSNR, UBS’s uMINT, Spiko’s currency products, Theo’s thBILL and dozens more.

Builder Perspectives: The Momentum is Real

We reached out to builders across the RWA stack to gauge where the industry stands on tokenization and yield bearing assets. The conversations spanned different layers: DeFi protocols deep in the trenches, specialized networks like Canton building infrastructure specifically for RWAs, tokenization platforms like Mu Digital, KAIO and Spiko and advocacy organizations like the Tokenized Assets Coalition working to advance the broader tokenization movement. Their perspectives paint a picture of an industry moving from experimentation to execution.

The Tokenized Assets Coalition sees the transformation firsthand. The inbound interest tells the story: major TradFi players and fintechs now proactively reach out for guidance on tokenization strategy and connections to leading projects. This marks a sharp reversal from 2022 when TAC was conceived and institutional players viewed key crypto projects as little more than toys.

Concrete milestones validate the shift. Securitize announced plans to go public at a $1.25 billion valuation. Figure completed its public listing. But TAC identifies the real catalyst: passage of the GENIUS Act in July served as the starter pistol institutions needed to incorporate stablecoins into their businesses. The next phase begins when rule-making around GENIUS gives compliance teams at major banks clear guidelines. This matters because stablecoins will provide liquidity for all forms of onchain RWAs.

Where does the real innovation lie? Not in simply putting money market funds onchain. The excitement centers on emergent assets and strategies that flow into programmable, interoperable DeFi infrastructure. The industry is barely in the first inning with significant infrastructure still needed. A critical gap remains: while yield bearing asset looping experiments show promise, the space desperately needs better transparency around collateral backing and holistic risk assessment of these strategies.

The shift toward utility is becoming visible. BlackRock’s BUIDL, tokenized through Securitize, is now accepted as collateral on Crypto.com and Deribit. VanEck’s VBILL fund is available as collateral on Aave Horizon. These examples show regulated, tokenized assets moving through CeFi and DeFi and connecting traditional market infrastructure with onchain finance.

Canton Network remains one of the most under-the-radar players in crypto-native circles despite being among the most serious tokenization infrastructure builders operating today. The privacy-enabled public blockchain processes over $350 billion in U.S. Treasury repo transactions daily and hosts over $6 trillion in tokenized assets across 400+ institutions. Goldman Sachs, BNY Mellon, DTCC, Circle, and major banks run production applications on Canton’s infrastructure, not pilots. While retail attention focuses elsewhere, the institutional build continues at scale.

The weekend Treasury financing execution Mathieson references demonstrates what institutional adoption actually looks like: real, regulated assets moving and settling atomically outside traditional market hours. Product-market fit crystallizing around solving concrete operational problems rather than chasing narratives.

Mu Digital represents one of the most prolific tokenization platforms focused on Asia-Pacific markets, a region that has remained largely opaque to global crypto capital despite representing over $20 trillion in credit opportunities. The platform is bringing Asian institutional yields onchain with a launch on Monad, the upcoming high-performance Layer 1.

Hizon cuts to the core problem: Asia’s best investments are gatekept to the financial elite. High minimums, multiple middlemen, limited cross-border deal flow. The barriers are stacked against everyday investors. Mu Digital changes this by bringing institutional-grade Asian credit onchain. The platform tokenizes the full spectrum of Asian credit investments: government-backed bonds, corporate debt, and private credit co-underwritten with blue-chip investment banks.

Spiko stands as one of the most profound and best-positioned tokenization platforms in the EMEA region, having launched Europe’s first fully tokenized money market funds approved by France’s AMF. The platform has scaled to over $400 million in AUM within its first year through entirely organic growth, processing more than $900 million in working capital from 1,000+ businesses.

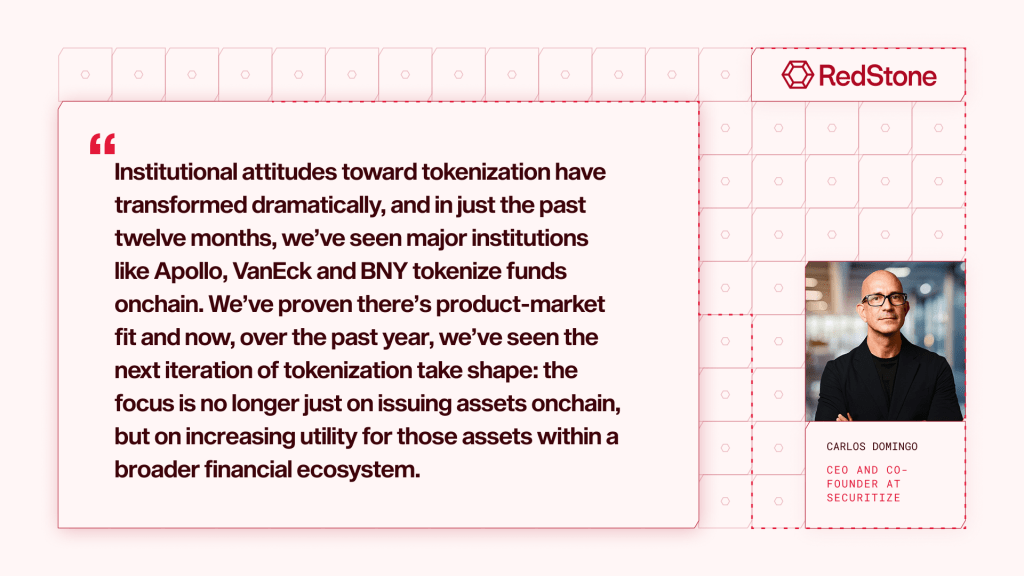

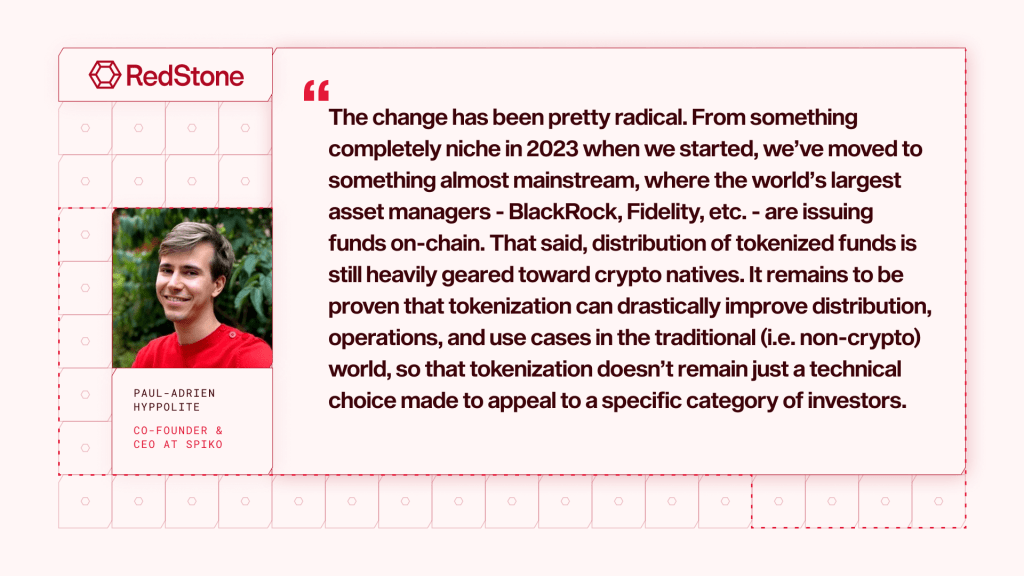

Hyppolite’s perspective carries measured optimism. Yes, the shift from 2023’s niche experiments to BlackRock and Fidelity launching onchain funds marks radical change. But with trillion-dollar projections flooding in from consulting firms and institutions, the real question is whether tokenization can deliver on the hype. Can it fundamentally transform traditional finance operations and distribution, or does it remain primarily a technical feature appealing to crypto-native users? That verdict is still pending.

KAIO had a breakout year in 2025, establishing itself as a leading institutional-grade tokenization platform. The protocol brought major traditional finance funds onchain: BlackRock’s ICS US Dollar Liquidity Fund, Brevan Howard Master Fund, Hamilton Lane’s Senior Credit Opportunities Fund, and Laser Digital’s Carry Fund. While currently focused on institutional and accredited investors, KAIO is moving toward opening access to standard crypto and DeFi users seeking regulated TradFi exposure through composable infrastructure.

The DeFi Multiplier Effect

In traditional finance, yield is usually the end of the journey. Capital is deployed, income is earned, and the cycle concludes. In decentralised finance, yield plays a different role. It is not the destination, but a building block that can be reused, collateralised, and layered across protocols.

This is possible because DeFi is composable. Protocols connect, and assets retain their utility wherever they move. Productive assets remain liquid, transferable, and in many cases permissionless, allowing capital to work in several places at once.

A simple example illustrates this. In a traditional system, staking ETH would lock capital and earn passive, fixed-term income and that is where the economic cycle ends. In DeFi, staked ETH becomes liquid staked ETH (for example, wstETH on Lido), which continues to earn staking rewards while remaining usable across the ecosystem. That wstETH can be supplied to a lending protocol, used to borrow stablecoins, and the borrowed capital redeployed to accumulate additional ETH or gain exposure to other assets such as BTC. Here, yield does not conclude the process. It fuels a recurring loop of productive use.

More advanced mechanisms extend this logic. Building on the previous example, a protocol such as Pendle allows a holder to separate wstETH into a principal token (PT-wstETH) and a yield token (YT-wstETH). The principal token can serve as collateral in a lending market, while the yield token can be traded. A single productive asset becomes collateral, a cash-flow instrument, and a trading primitive simultaneously.

A similar transition is now taking place with stablecoins. Historically, stablecoins functioned as static settlement assets. Today, yield bearing versions allow a dollar to generate yield, and simultaneously be used in liquidity pools or as collateral. This unlocks capital-efficient cash management strategies and extends the productive-asset model beyond volatile tokens such as ETH and SOL.

The key point is simple: composability multiplies what productive capital can do. In DeFi, yield bearing assets are not just held for return. They circulate, secure lending markets, act as collateral, and power liquidity and settlement flows. Each movement reinforces market depth and capital efficiency. Because of this, yield bearing assets are shifting from performance instruments to infrastructure, forming the collateral base, settlement layer, and reserve foundation of an increasingly institutional onchain economy.

DeFi Runs on Yield Bearing Assets.

This shift across YBA classes is reinforced by money market adoption. Liquid staking assets now make up substantial portions of major lending protocols: SOL LSTs represent roughly 30% of Kamino’s TVL, while ETH LSTs account for nearly 30% of Aave V3’s TVL. These figures demonstrate that YBAs are already integrated into core market functions and are becoming foundational to DeFi.

Source: Defillama

Source: Defillama

Interestingly, institutions have become central to the rise of YBAs rather than passive observers.

BlackRock’s BUIDL fund has brought tokenised U.S. Treasuries directly to public blockchains, with secondary wrappers such as sBUIDL enabling composable deployment across lending and liquidity layers. Coinbase integrated Morpho’s institutional lending vaults (a product line that has already surpassed USD 11 billion in deposits), enabling regulated capital to operate under curated risk frameworks. Franklin Templeton continues to expand tokenised money-market infrastructure, while Ondo has emerged as a major gateway connecting traditional fixed-income instruments to DeFi liquidity venues.

These developments mark an inflection point. YBAs are not being adopted because they offer “crypto yield”, but because they mirror institutional liquidity behaviour and improve upon it via programmability, real-time settlement, and composability. For institutions, the appeal is straightforward: cheaper, more efficient and more productive capital.

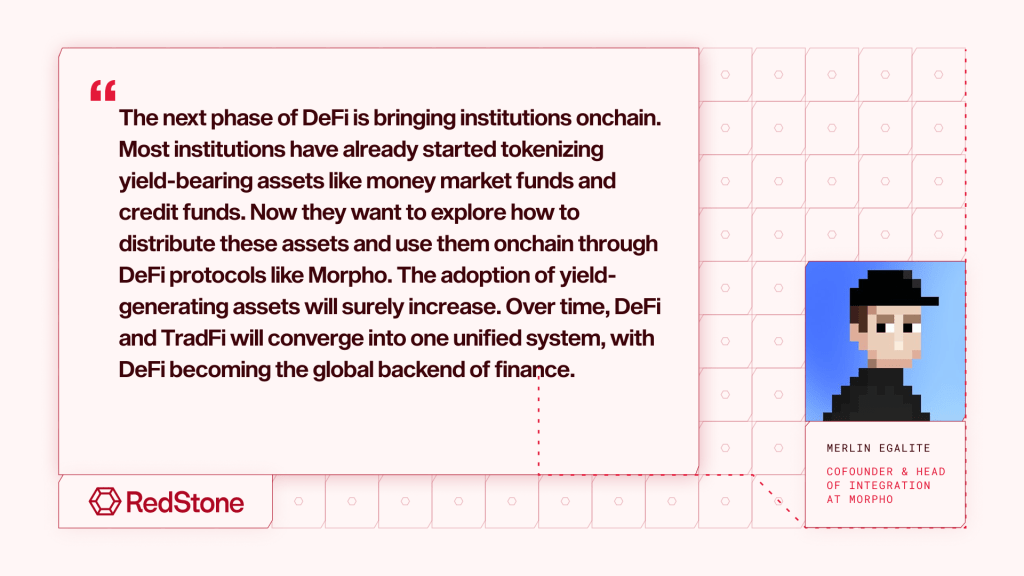

The next phase of growth depends on strengthening this foundation. Expansion will come through deeper DeFi integration and institutional-grade infrastructure, a movement already underway as protocols such as Morpho and Lido offer tailored solutions for enterprises and regulated entities.

As well as platforms like OpenTrade, which are purpose-built for institutional use from the ground up. OpenTrade enables companies to launch their own stablecoin yield products, backed by enterprise-grade technology, time-tested legal protections, and bank-grade asset management.

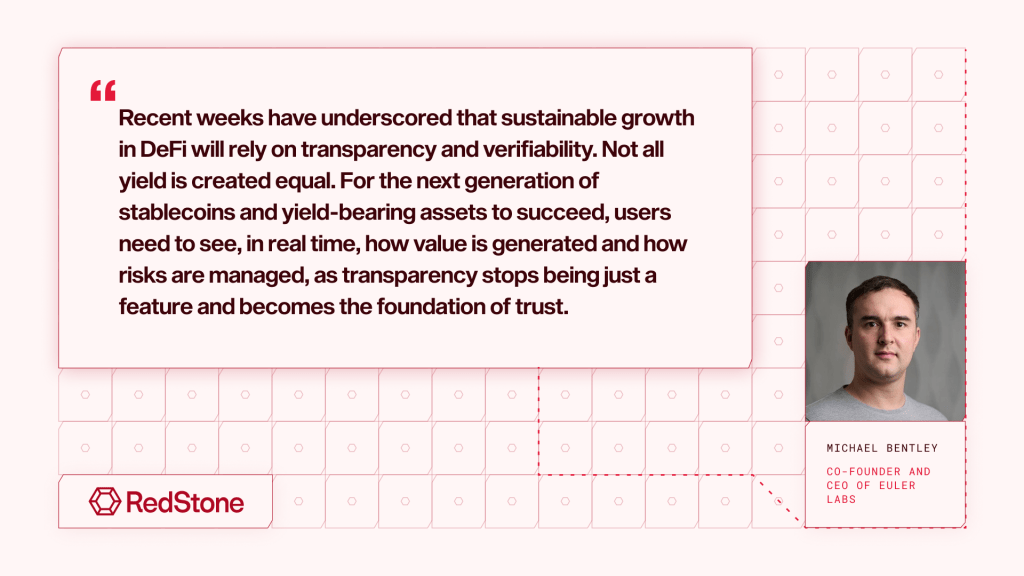

Yet institutions do not adopt products alone; they adopt standards and guarantees. As YBAs scale, risk management, clarity on yield sources, and collateral curation become essential. The question shifts from how to generate yield to how to qualify, secure, and scale productive collateral responsibly.

The following section explores this transition and why the ability to curate and tier collateral will determine which yield bearing assets become the backbone of institutional DeFi.

Curation to Stimulate Institutional Adoption

YBAs and their composability allow productive capital to circulate across multiple layers of DeFi. This unlocks efficiency, but it also means that risk can compound across layers if not properly managed. Curation is therefore not a limitation on innovation. It is what allows innovation to scale safely and become investable at institutional standards.

In early DeFi markets, risk assessment focused on volatility, liquidity depth, counterparty exposure, and oracle integrity. With YBAs, the evaluation surface is even broader. These instruments embed cash flows, redemption mechanics, and layered economic exposure, requiring more active and multifaceted curation.

This makes the curation of YBAs structurally more complex than vanilla tokens. Several characteristics must be addressed when assessing these assets:

Multi-layer economic exposure

Liquid-staking tokens, restaked assets, and yield-split tokens can simultaneously represent staking income, slashing risk, restaking obligations, and derivative layers. This layering increases efficiency, but also concentration and tail-risk if not managed carefully.

Liquidity and redemption mechanics

Some YBAs benefit from immediate liquidity and deep secondary markets. Others rely on queued withdrawals or delayed redemption cycles. A token with real-time convertibility is fundamentally different from one with staged exit rights, and curation reflects this by assigning differentiated collateral power.

Yield provenance and durability

Institutional allocators assess the source, reliability, and sustainability of yield. Staking rewards, Treasury yields, funding spreads, and incentive-driven returns carry distinct risk profiles. Curated collateral frameworks require transparent yield sources and avoid reflexive or opaque structures.

Pricing and oracle design

Accrued yield affects the principal value of YBAs. Pricing feeds must accurately reflect both, or collateral inflation and mis-stated solvency can occur. YBAs therefore demand robust oracle standards and clear valuation logic.

Curation in Practice

To address these complexities, leading protocols are adopting structured mechanisms that resemble institutional risk frameworks:

Isolated collateral architecture

Morpho vaults, Kamino vaults, Euler isolated markets, and Aave v3/v4 isolation modes confine risk and prevent cross-market contagion.

Differentiated collateral parameters

Loan-to-value ratios, liquidation thresholds, and supply caps are calibrated separately for LSTs, restaked assets, structured yield products, and tokenised treasuries.

Specialised risk stewards

Firms such as Gauntlet, Steakhouse, Re7, and MEV Capital conduct ongoing stress-testing and dynamic parameter adjustment across billions of dollars in collateral. Their function resembles institutional credit-risk and collateral management desks, not discretionary asset managers.

Transparency and operational standards

Protocols increasingly require clear disclosure of redemption mechanics, valuation methodology, oracle design, custody assumptions, and operational risks prior to collateral onboarding, aligning with institutional disclosure and due-diligence practices.

What Does Curation Enable?

Curation is not a brake on DeFi. It is the system that allows productive capital to scale safely. Institutions will not adopt at scale collateral environments that are unbounded or experimental. They require predictability, controlled leverage, and clear liquidation rules.

If composability turns assets into productive capital, curation ensures that capital can support lending markets, settlement layers, and reserves with confidence. Strong curation frameworks will determine which YBAs evolve from novel instruments into institutional-grade financial infrastructure capable of scaling onchain finance into a trillion-dollar industry.

The DeFi Flywheel in Motion

Let’s now bring the previous concepts together through a concrete example that shows composability in practice. The journey of sUSDe demonstrates how a single yield bearing asset can move through multiple layers of DeFi, generating yield, creating tradable rate markets, and unlocking new credit capacity.

The YBA’s Foundation (sUSDe)

Ethena’s USDe is a synthetic dollar backed by BTC, ETH and staked ETH collateral and hedged through perpetual futures. This delta-neutral model captures two yield streams (staking rewards from the collateral and funding rates from the futures position) while maintaining a stable dollar value.

From this structure, sUSDe emerges as the yield bearing version of USDe, distributing the combined yield directly to holders. In practice, sUSDe functions as an on-chain money-market instrument: it tracks one dollar in value, remains liquid and transferable, and continuously accrues return.

For institutional investors, this represents a crucial evolution. sUSDe behaves like a short-duration instrument or tokenised T-bill fund, but operates natively within DeFi. It can be held as a treasury asset, supplied to liquidity pools, or used as collateral without losing its productive status.

The Rate Layer (Pendle Integration)

Once obtained, sUSDe can be deposited into Pendle, a protocol that allows users to separate the asset’s principal value from its future yield. Pendle has been widely used in DeFi and has become one of the blue-chip products for the wide ecosystem – with $13 billion TVL at its peak in September 2025, and ~$6 billion as of November 2025.

In the case of Ethena, Pendle converts the deposit into two components:

- PT-sUSDe (Principal Token): represents ownership of the underlying asset, redeemable at maturity for its face value.

- YT-sUSDe (Yield Token): represents the right to claim the yield generated until maturity.

This split effectively tokenises the time value of money. Investors seeking fixed returns can buy or hold the PT, locking in a predictable yield. Others can trade YTs to speculate on or hedge future rate movements.

The interaction between PT and YT forms a transparent, continuously priced on-chain interest rate curve. It reflects how market participants value future yield streams, similar to how bond markets establish forward rates.

PT tokens are widely adopted as collateral assets in lending markets, predominantly for lucrative looping strategies – for example, PT-sUSDe looping on Aave, Morpho, or Euler. For these markets to operate efficiently and prevent bad debt accumulation, an efficient oracle methodology for pricing PT tokens is essential. RedStone and Objective Labs have created a bespoke research and PT-oracle pricing product that enables such markets to scale effectively. The methodology is based on the principle that PT tokens function like zero-coupon bonds in traditional finance: they trade at a discount to their face value and converge toward it as the maturity date approaches. The methodology ensures real-time accuracy, as pricing is based on live blockchain data and Pendle’s internal mechanics. It can help scale PT-oracle-powered markets to tens of billions of Dollars securely. The full implementation will be revealed during the Ethereum DevConnect conference in Argentina.

The Credit Layer (Morpho Vaults)

The PT-sUSDe, which now represents a stable principal with a known redemption value, can be further deployed in Morpho, a modular lending protocol designed for curated, risk-tiered credit markets.

Morpho allows lenders and borrowers to interact through isolated vaults, each governed by specific risk parameters such as loan-to-value ratios, liquidation thresholds, and collateral caps. These parameters are managed by independent risk stewards (firms like Gauntlet, Steakhouse, or Re7) who continuously monitor volatility, liquidity, and systemic exposure.

By depositing PT-sUSDe as collateral, users can borrow against their position or extend credit to others in a controlled environment. This process mirrors traditional markets, where safe assets like Treasuries are used to secure short-term funding.

At this layer, yield bearing collateral is fully integrated into DeFi’s credit infrastructure. The same dollar of productive capital that originated in Ethena’s yield layer and was split on Pendle now supports lending activity, market liquidity, and credit formation, all within transparent, programmable boundaries.

Stacking the DeFi legos back up

This flow ETH > stETH > USDe > sUSDe > PT/YT > Morpho encapsulates the composable balance sheet of decentralised finance. It shows how a single yield bearing asset can act as cash, fixed income, and credit collateral in one continuous system.

Yield bearing assets no longer represent passive holdings, they have become the financial infrastructure powering a self-reinforcing, institutional-grade on-chain economy.

Note: This section has been authored by DL Research.

Summary

Yield is the foundation of finance. TradFi risk models, asset valuations, and investment frameworks all center on it. As crypto shifts into its infrastructure role, yield bearing products issued on blockchains will scale to meet this constant institutional demand.

Growth will span every category. In mature markets, yield bearing assets consistently outperform non-yielding alternatives. Yield bearing stablecoins, liquid staking on crypto blue chips, tokenized real-world assets, and DeFi composability layers stacking returns across protocols. The pieces are moving into place, and the appetite for yield never diminishes.

This is the future RedStone and Credora are building toward. Infrastructure that enables the most secure, reliable, and scalable oracle services and standardized DeFi risk evaluation with transparent performance metrics, all with institutional-grade reliability. The onchain economy is heading to a trillion-dollar scale. What separates winners is who builds the rails to get there.

Stay tuned for this comprehensive analysis – follow us at https://x.com/redstone_defi and sign up for our monthly newsletter at https://redstone.finance/ to ensure you don’t miss it when it drops!

Authors

RedStone is a modular blockchain oracle specializing in yield bearing assets for DeFi and onchain finance, especially value-accruing stablecoins, Liquid Staking and Restaking Tokens. It offers secure, reliable and customisable data feeds across 110+ chains. Trusted by Securitize, Ethena, Morpho, Drift, Compound, ether.fi, Lombard and more.

Credora consolidates creditworthiness data, default probabilities and collateral analytics into a unified ratings layer for onchain finance. Users of DeFi protocols like Morpho or Spark, can compare vault and loan positions by relative risk scores, which is a key factor for institutional investors looking to explore tokenized treasuries, private credit and structured DeFi products.

Gauntlet provides optimization strategies for digital assets, protocols, and blockchains. Gauntlet equips investors, builders, and token issuers to manage funds onchain by leveraging the most trusted economic models in crypto.

Stablewatch is a leading analytics platform for stablecoins and yield bearing stablecoins. It delivers real-time and historical data on vaults, RWAs, tokenized deposits, and yield bearing assets. Tracking over 60 assets and more than $20B in total value, Stablewatch enhances transparency across onchain finance through historical APY, TVL, and risk analytics.

The Tokenized Asset Coalition (TAC) is a 501(c)(6) member-funded non-profit corporation on a mission to onboard the next trillion of assets onchain. The TAC’s members account for over $100B of combined market cap and onchain value. The TAC’s member dues fund initiatives to educate and advocate for best practices for building the onchain infrastructure of tomorrow.

DL Research is an independent news organisation that provides in-depth reporting on the largely misunderstood world of cryptocurrency and decentralised finance. From original stories to investigations, our journalism is accurate, honest and responsible.

Core contributors to the report:

- Marcin Wilk, Research Analyst at RedStone

- Marcin Kazmierczak, Co-Founder at RedStone

- Gil Santos, Quantitative Engineer at RedStone

- Johnny Reisch, Executive Director at Tokenized Asset Coalition

- Piotr Kabaciński, Head of Research at Stablewatch

- Maksymilian Łucykiewicz, Marketing Lead at Stablewatch

- Simon Mathonnet, Product Marketing Lead at Gauntlet

- Jake AuJus, Senior Protocol Strategist at Gauntlet

- Sebastien Nave, Data and Research Analyst at DL Research

References

- The official documentation for all the described projects

- DeFiLlama. Analytics Platform. Accessed 2025. https://defillama.com

- Ocorian. “Value of Global Assets Hits Record $248.8 Trillion Driven By Surge in Equities.” Knowledge Hub. Accessed 2025. https://www.ocorian.com/knowledge-hub/insights/value-global-assets-hits-record-2468-trillion-driven-surge-equities

- TechSci Research. “Bond Market Report.” Accessed 2025. https://www.techsciresearch.com/report/bond-market/27048.html

- Nareit. “REITs by the Numbers.” Data & Research. Accessed 2025. https://www.reit.com/data-research/data/reits-numbers

- Token Terminal. “Staking Market Cap.” Accessed 2025. https://tokenterminal.com/explorer/metrics/staking-market-cap

- Staking Rewards. Accessed 2025. https://www.stakingrewards.com/asset/solana/analytics

- Stablewatch. Analytics Platform. Accessed 2025. https://www.stablewatch.io/

- Artemis Analytics. Analytics Platform. Accessed 2025. https://app.artemisanalytics.com/