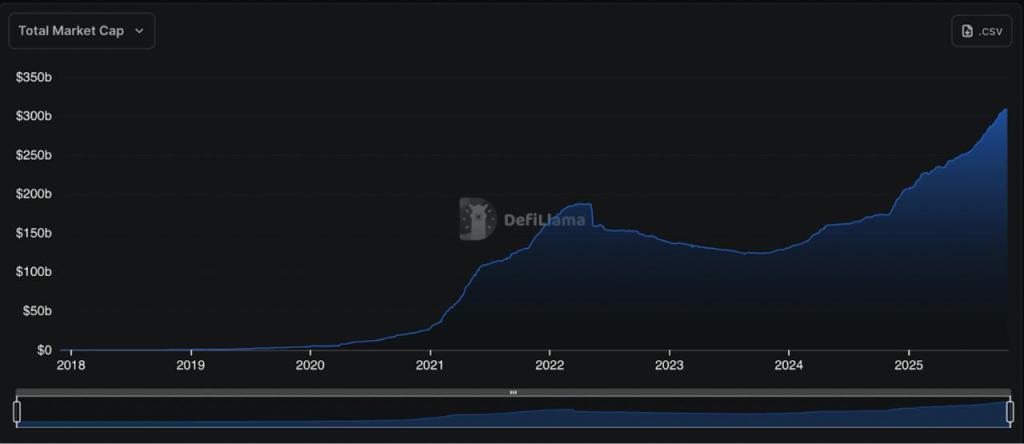

Crypto added more than one hundred billion dollars of stablecoins between January and November 2025, a 50% expansion in under ten months, amounting to $307 billion. Stablecoins are the fastest growing vertical in crypto, and are widely treated as the safest corner of the market. They are the quiet denominator beneath everything else.

Every derivative, lending market, liquidity pool, and cross-chain settlement rests on a simple expectation: that a stablecoin will trade close to its target value. Most reference the U.S. dollar, but what DeFi protocols actually use is the market price delivered by oracles, not a blanket promise of fiat redemption.

For fiat-backed coins, redemptions help anchor that price. For crypto-backed or synthetic models, mechanisms such as auctions, collateral ratios, or strategy NAVs play the same role. When the market price drifts too far for too long, the shock ripples through every protocol built on top of it. In practice, it’s the oracle-tracked price that determines how far that stress travels.

This article examines how stablecoins maintain that one-dollar promise, and why, at times, they fail to hold it.

How USD-Denominated Stablecoins Stay at One Dollar

A stablecoin is a crypto asset engineered to track a stable reference. Unlike BTC or ETH, they aren’t designed to appreciate; they’re designed not to move.

Most stablecoins follow one of three designs:

- Fiat-backed – Each token is backed by a portfolio of assets held by the issuer, typically cash, short-term U.S. Treasuries, commercial paper, or other liquid instruments. The peg holds because users believe redemption will clear at one dollar, and that belief is reinforced by the issuer’s track record, transparency reports, and brand credibility.

- Crypto-backed (onchain overcollateralized) – Coins like USDS (prev. DAI), GHO or LUSD are backed by on-chain assets such as ETH, BTC or LSTs. These models are transparent and resilient, but efficiency and scalability are the biggest bottlenecks.

- Synthetic / hedged strategies – Newer designs use delta-neutral or hedge-fund-style trading strategies on assets. These attempt to keep the peg by actively managing risk rather than holding fixed, pre-defined reserves.

Why the Market Price Usually Returns to One Dollar (Most of the Time)

Stablecoins do not trade at $1 because someone enforces the sticker price. They cluster around $1 because arbitrage makes mispricing costly to ignore. If a coin trades at $0.98 but can be redeemed for $1, a trader buys at $0.98 and redeems until the spread closes. It might not sound like much, but scaled across tens of millions of dollars, that tiny spread becomes meaningful, and for specialized market makers, it’s effectively risk-free, assuming no black swan events intervene. In equilibrium, profit-seeking keeps the peg, not decree. This mechanism implicitly assumes two legs continue to function: (1) redemption is possible and (2) liquidity exists to express the trade.

Two Species of Depeg

Not every depeg is a disaster.

- Temporary depegs: Reserves are sound; the market is just dislocated or thin. Arbitrage or restored confidence pulls price back.

- Structural depegs: A real constraint breaks: collateral is gone, redemptions halt, or the design collapses on itself. Without external capital or an emergency policy, price cannot close the gap.

This is the difference between a stress impulse response and a terminal state.

Common Root Causes

Across incidents, the same stressors recur:

- Reserves frozen, seized or inaccessible

- Forced liquidations cascading through volatile collateral

- Design assumptions (LTV, leverage, correlations) breaking under stress

- Oracle distortion mis-pricing collateral or liabilities

- Opacity triggering endogenous bank runs on fear alone

Different narratives, same mechanical pathways.

The Stakes Scale With Market Size

Stablecoins are the denominator of DeFi. Lending is quoted in them. Perps settle in them. Payment rails coordinate on them. A depeg in one stablecoin does not stay “local”; it propagates upward into every surface layer priced against it. The more complex the products built on top of stablecoins become, the more hidden risks they introduce. Which means the only thing that actually protects the system is live measurement, not post-mortem diagnosis after the damage is done.

From Heuristic Trust Toward Rated Transparency

For most of crypto’s lifespan, markets priced stablecoin risk by reputation and vibes. That interface breaks when capital is institutional and designs are reflexive. A mature market needs resilience that is rated, not asserted; stress-observable in real time, not inferable only after collapse.

S&P Global’s initial work on stablecoin resilience showed the market wants something beyond reputation. The next step is to bring that discipline onchain and with crypto-native latency. RedStone’s acquisition of Credora enables us to rate stablecoins and stablecoin strategies directly, in real time. The intent is to replace narrative trust with monitored evidence that markets can price immediately, because stability strengthens when risk is measured continuously, not assumed.

September’s announcement of RedStone acquiring Credora Network. Source: RedStone blog.

Why the Oracle Layer Determines Whether Stability is Observable

RedStone underwrites around 97.9% of stablecoin market coverage, powering both market and fundamental data for the assets that anchor DeFi. Stablecoins rely on accurate reference points: the market rate that reflects current trading activity and the fundamental rate that represents the value of their underlying reserves.

RedStone delivers both in real time, providing precise feeds for secondary market pricing and onchain access to issuer-reported NAVs.

Without correct and timely data, arbitrage breaks, liquidations misfire, and what should be temporary stress can evolve into structural failure.

In stablecoin markets, the oracle is not an accessory, it is the part of the machine that tells you if the machine is still working.