Highlights

- Staking, originally intended as a stable and predictable primitive, has evolved into one of the most innovative and rapidly expanding sectors in the crypto industry, with Ethereum remaining the central hub of this ongoing evolution.

- Ethereum Staking and Liquid Staking marked Phase 1 of fundamental yield creation in the crypto industry. In 2024, the Restaking and Liquid Restaking boom represents Phase 2. What’s key is that Restaking further fuels staking growth, as LST assets are the primary ones being restaked on platforms like EigenLayer, Symbiotic, Karak, and others.

- RedStone, in collaboration with CoinDesk Indices, has launched a CESR (Composite Ether Staking Rate) oracle feed on Ethereum – the first on-chain, fully standardized Ethereum Staking Rate benchmark, potentially serving as the backbone for a new wave of DeFi primitives focused on Ethereum yield derivative products.

- Although Staking and Restaking may appear similar at first glance, they are distinct primitives with different dynamics and risk factors. Staking involves homogeneous risks tied to ETH, while Restaking introduces heterogeneous risk profiles unique to each AVS, including liquidity, slashing conditions, and technical risks.

- The Staking landscape is rapidly growing and innovating, driven by capital efficiency, market maturity, liquidity, and rising institutional demand from the approval of Ether ETFs.

Ethereum Staking Landscape

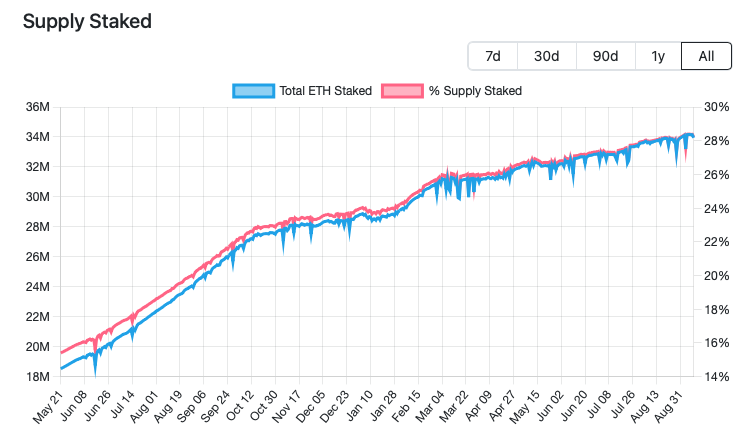

Over the years, staking has increasingly become a cornerstone in the design of blockchain technical principles. Today, it stands as one of the most battle-tested modules of blockchain infrastructure, widely recognized as a more environmentally friendly and economically viable consensus algorithm in the long run in contrast to Bitcoin’s Proof of Work schema. While Proof of Stake (PoS) has many facets and caveats, this report will focus on Ethereum, which is the largest PoS blockchain by total value secured. As of September 9, 2024, Ethereum’s security budget amounts to a staggering $80 billion worth of ETH, representing roughly 29% of the total ETH supply. The Ethereum staking landscape, with staked Ether being dubbed as an Internet-native bond, has experienced significant second-order effects stemming from its early design choices over the past few years. These include the introduction of Liquid Staking and, subsequently, the Liquid Restaking category, which have led to an unexpected linear increase in the staking rate. These events have shaped staking into the most successful and enduring sub-category of Decentralized Finance. However, there is growing concern among researchers that the tremendous adoption success and rapid expansion of the hyper-tokenized staking industry could lead it to become a victim of its own success. Consequently, some are advocating for reconsideration of Ethereum’s issuance policy.

This report aims to illustrate how fundamentally new primitives have reshaped the once-stable staking landscape. To achieve this, we need a reliable benchmark that tracks the average Ether yield across the broader ecosystem to accurately assess the changes in various staking yields. CoinDesk Indices’ CESR (Composite Ether Staking Rate) is perfect for this, aggregating the average yield across the Ethereum validator population. CESR provides participants in the Ethereum ecosystem with a standardized benchmark rate for staking.

We are thrilled to announce that CESR is now available on-chain through RedStone, making this the first-of-its-kind, institutional-grade solution that enables builders to access reliable data on the aggregated staking rate to create innovative products!

The Ever-Changing Staking Market

The staking landscape is often associated with stability. At its core, it’s a straightforward primitive: one agrees to follow the protocol’s rules by running a node instance with an attached economic stake, known as a validator and agrees to the slashing conditions. Slashing occurs if undesirable actions, such as a double-spend attack, are performed or if agreed-upon tasks, like timely block attestation, are not fulfilled. In return, an active validator receives variable rewards consisting of new ETH issuance, MEV (marginal value captured from reordering user transactions within a proposed block), and priority tips from end-users for faster transaction finalization. Collectively, this reward rate is called the staking yield.

Note that rewards have been steadily declining over the past two years, as reflected in the CESR rate. The primary reason for that, apart from decreasing L1 activity due to the rollup-centric roadmap, is ever-increasing demand for staked Ether. Naturally, individual staking returns will decrease as more participants share the same reward pool.

The first staking boom is attributed to the concept originally known as Delegation Vouchers, now widely recognized as Liquid Staking. The ability to outsource the technical burden of being a validator to a specialized entity, while still receiving the majority of validator rewards, was crucial in boosting the much-needed staking adoption to ensure the underlying security assumptions of the Ethereum network. This also served to practically demonstrate the concept of PoS-backed blockchain security, which, when the Ethereum Beacon Chain went live, was far from a consensus among crypto natives. Liquid Staking became so successful that it created a new dilemma: the majority of the stake ended up concentrated within Liquid Staking protocols, which are largely governed by their own communities through Liquid Staking Tokens (LSTs) like Lido. Some argue this has introduced a centralization risk, sparking an ongoing debate about the health of Ethereum’s staking landscape.

Building on the success of Liquid Staking, the industry took it a step further by outsourcing top-tier Ethereum security to external networks, creating mutual benefits for all parties involved. We’ll explore the details of Restaking in the further section, but for now, it’s worth noting that this primitive also became a significant success, drawing even more capital into the staking landscape. To illustrate, over the past year, EigenLayer and Ether.fi have joined the list of the top 5 DeFi protocols by TVL. The thing is, when Ethereum’s PoS system was being designed, no one anticipated such a success for this primitive. Originally, the staking rate was expected to be around 12.5-25%, but we’ve steadily surpassed that, now sitting at roughly 29%. Once again, the staking landscape and its dynamic market have surprised its architects. This has led some researchers to grow increasingly concerned about the long-term health of the system under the current fixed parameters, advocating for a reconsideration of Ethereum’s issuance policy. If such changes were proposed and implemented, it could theoretically flip the switch, altering the dynamics of the entire landscape once more.

CoinDesk Indices’ CESR Goes On-chain with RedStone

The staking landscape has grown into a massive industry worth tens of billions of dollars. Over the years, it has also paved the way for more financially complex products to meet the ever-increasing demand for exposure to the space. A prime example is Pendle, which has seen tremendous growth by capitalizing on the rising demand for Staking and Restaking yield derivatives, particularly offering novel LRTs and LRTs beta exposure.

RedStone, in collaboration with CoinDesk Indices, is excited to announce the launch of CoinDesk Indices’ CESR (Composite Ether Staking Rate) as a new and novel RedStone price feed. RedStone will deliver the updated CESR rate, starting with Ethereum Mainnet, in a Push model every 24 hours, enabling builders to create innovative DeFi primitives. CESR is a globally adopted, on-chain standardized Ethereum Staking Rate. With ETH’s ETF recently approved, legitimizing the asset and drawing increased attention from traditional finance, CESR can facilitate new primitives tailored for institutional players, such as on-chain interest rate swaps, staking rate derivatives, staking rate insurances, yield-curve products, and fixed-income markets.

If you’re interested in building with the CESR, be sure to check out the RedStone Push Model documentation section!

How Has Restaking Changed the Playing Field?

When we think of Restaking, EigenLayer immediately comes to mind. EigenLayer is the protocol that popularized the concept, allowing ETH or liquid staking token (LST) holders to reuse their staked assets by opting into the EigenLayer schema. This approach extends cryptoeconomic security to additional applications, Actively Validated Services (AVS) like rollups, RPCs, data availability, oracles, and more, offering users extra rewards. We don’t have the space to delve into the broader concept of Restaking or its technical implications within the crypto landscape, but we’ll focus on how Restaking is fundamentally different from anything we’ve seen before in terms of economics, how it’s changing the Staking game, and the dependencies on third-party protocols, known as Liquid Restaking protocols, which specialize in simplifying access to Restaking returns.

Restaking, at its core, is an opt-in process. It’s not just about deciding whether to participate in Restaking or stick to vanilla Staking, it requires users to choose which specific new networks they want to restake their assets to. To put this in perspective, let’s look at the well-known Liquid Staking market. Essentially, all Liquid Staking protocols perform the same task, validating Ethereum consensus. As a result, as seen with CESR, there’s not much variance between validators, making a simple mathematical tool like the mean ideal for illustrating overall performance. However, with Restaking, you can take on multiple jobs (choosing from a broad range of Actively Validated Services), but each of these jobs has a significantly different risk profile. This means that every validated AVS might offer a different yield and carry a different risk level. If you decide to support multiple services, you end up with a unique combination of underlying yields and risk assumptions. In essence, this introduces a new dimension to the staking equation, knowledge about the technical and financial risks each AVS presents, and the ability to quantify them, making Restaking an order of magnitude more complex than traditional liquid Staking. To summarize, the risk profiles in Staking can be described as homogeneous (all based on the same underlying asset – ETH), while Restaking introduces heterogeneous risk profiles (specific to each AVS, including factors like outstanding liquidity, slashing conditions, technical risks, etc.). If you want to dive deeper into quantifying the potential risks of each platform, Gauntlet’s EigenLayer Risk Dashboard is a great resource.

Given all this, it’s clear that Liquid Restaking protocols (LRTs) are even more essential as middlemen in Restaking than they were in pure Staking. These LRT protocols, much like hedge funds, combine market and technical expertise to simplify the process for users by managing:

- The operational risks associated with each operator

- Which Actively Validated Services (AVSs) the operator supports

- Stake optimization (how much stake the operator delegates across different AVSs)

With the strong narrative driving the Restaking movement over the past year, the rapid growth of LRT protocols is well justified, even to the point of eating into the market share of LST players like Lido and Rocketpool.

Since Restaking platforms aren’t fully operational yet, particularly lacking payments and slashing implementations, it’s too early to evaluate their direct impact on underlying ETH yields. However, it’s certain that the variance and risk profiles – think traditional finance metrics like the Sharpe Ratio will differ significantly between various Ether Restaking derivatives. This presents an exciting opportunity for another wave of innovation within the industry.

At RedStone, we’re deeply involved in this space, even building as an AVS ourselves. We’re gearing up for the next edition of the Restaking Landscape report, which will be released in the coming weeks – stay tuned!

Is Ethereum Truly an Internet Bond?

Traditionally, bonds, especially national ones, have been seen as a robust and safe asset class, backed by the solvency of the issuing country—for instance, US Treasuries backed by the US Government. With the recent approval of ETH ETFs, many traditional institutions are now crafting a narrative around Ether. Interestingly, what was once a fully crypto-native idea – ETH being an “Internet Bond” has been embraced by traditional finance, with agencies like Bloomberg and S&P Global promoting it as an excellent index for exposure to blockchain innovation.

This narrative makes for a compelling investment story, but it’s important to remember that none of the approved ETFs have been granted permission to stake the underlying asset, making Ether a bond without a coupon for ETF investors. However, many believe that this could change, and Ethereum staked ETFs may eventually be available for trading in the US. It’s worth noting that traditional investors often favor yield-bearing assets, which can be evaluated using well-established metrics like P/E or EPS ratios. This is much harder to achieve with an asset like Bitcoin, which lacks a protocol-embedded staking yield embraced by all participants. Returning to the CESR rate, we now have over three years of yield data, demonstrating it as a robust and stable earnings alternative. Even though the price of Ether has fluctuated significantly during this period, members of the relatively new class of crypto institutional buyers tend to focus less on short-to-mid-term price movements and more on multi-year timeframes, as ETFs are primarily long-term investment vehicles.

Closing Thoughts

With each passing year, the crypto industry becomes increasingly embedded in mainstream finance. Ether staking and its yield by-products have been, and continue to be, hotspots for infrastructure and DeFi innovation. The future looks particularly promising for the staking industry, given its capital and ecological efficiency, mature market stage, abundant liquidity, and legitimacy, along with the new wave of institutional demand sparked by the approval of Ether Exchange-Traded Funds (ETFs). However, we must remember that the constant rate of innovation is a double-edged sword – it can introduce new, disruptive risk factors that haven’t been fully explored. The rapid rise of Restaking as a major part of the Staking landscape could lead to unforeseen second-order effects that weren’t anticipated in the initial design. Additionally, there are ongoing discussions about the sustainability of solo validators and potential changes to Ethereum’s issuance curve, which could alter the underlying structure. Yet, the Ethereum ecosystem remains strong, with numerous teams and thousands of individuals working daily to improve and ensure the well-being of this collectively-owned, meritocratic, open-source protocol that Ethereum and together with its L2s have undoubtedly become.

We’re incredibly excited to introduce another missing piece of the Staking puzzle by bringing the CESR oracle, in collaboration with CoinDesk Indices – the first on-chain, fully standardized Ethereum Staking Rate. This could serve as the backbone for a new wave of DeFi primitives, meeting the growing demand for novel, sophisticated products like loan/bond-based offerings and Ethereum yield derivatives!

CoinDesk® and the Composite Ether Staking Rate (CESR®) (the “Data”) are trade or service marks of CoinDesk Indices, Inc. (“CDI”), the publisher of the Data, and/or its licensors, including CoinFund Management LLC (“CoinFund”), the owner and administrator of CESR (collectively with CDI, the “Rate Providers”). The Rate Providers own all proprietary rights in the Data. The Rate Providers do not sponsor, endorse, sell, promote or manage any investment offered by any third party that seeks to provide an investment return based on the performance of the Data (“CESR Products”). CDI is neither an investment adviser nor a commodity trading adviser and the Rate Providers make no representation regarding the advisability of making an investment in any CESR Product. The Rate Providers do not act as fiduciaries with respect to any Products. A decision to invest in any Product should not be made in reliance on any of the statements set forth in this document or elsewhere by the Rate Providers. The Rate Providers do not guarantee the accuracy, completeness, timeliness, adequacy, validity or availability of any of the Data. The Rate Providers are not responsible for any errors or omissions, regardless of the cause, in the results obtained from the use of any of the Data. The Rate Providers do not assume any obligation to update the Data following publication in any form or format. © 2024 CDI and CoinFund. All rights reserved.