Ethena Origins: “Dust on Crust” By Arthur Hayes

Ethena Labs’s mission is to create a synthetic dollar that is not reliant on traditional banking rails. The team has developed USDe, a synthetic dollar that is fully collateralized using the mechanisms of the internal crypto economy, unlike USDT and USDC, which rely on external banks’ balance sheets. USDe stands as a significantly more multifaceted and innovative product than traditional fiat-backed stablecoins. This intro article attempts to demystify Ethena, presenting its uniqueness to end-users in plain English.

The sole concept behind Ethena and USDe riffs upon the idea first popularized by Arthur Hayes – crypto OG, investor and BitMEX co-founder. Around one year ago, Hayes wrote the Dust on Crust article regarding stablecoins and their purpose in the crypto market, as well as inefficiencies and drawbacks related to traditional finance. He addressed the existing stablecoins scaling ceilings and presented a concept for a stable token incorporating long spot and short perpetual swap positions. Hayes’s discussion focused on BTC, whereas Ethena leverages Ether, capitalizing on its unique properties like Liquid Staking to achieve a similar delta-neutral stance.

Ethena founder Guy Young has a strong background in traditional finance. Young embarked on realizing the concept, refining and enhancing it to address one of the most critical challenges in the crypto space: creating a liquid, scalable, and censorship-resistant synthetic dollar.

The ambition to establish a stable currency fully independent from the TradFi system represents a mountain that is indeed worth climbing. DeFi could truly unfold its potential and emerge as a parallel financial ecosystem with the widespread adoption of USDe. Ethena, in its end-state, might closely tackle the stablecoin trilemma, which demands three crucial attributes in a digital stable currency: price stability, decentralization (encompassing collateral custody, permissionless interaction, and transparency), and capital efficiency.

Ethena Overview: “The Internet Bond” Potential

Ethena’s USDe stands apart from traditional fiat-backed stablecoins like USDC and USDT or overcollateralized stables such as Maker’s DAI. Instead, it represents a synthetic dollar backed by crypto assets and corresponding short derivative positions. The Ethena protocol primitive is deployed on the Ethereum Mainnet only as of March 2024. Beyond its primary function of facilitating the USDe synthetic dollar, it introduces a yield-generating mechanism. This positions Ethena as a contender aiming to join the evolving narrative of an Internet Bond. Let’s delve into the Ethena and USDe mechanisms, examining each component to fully comprehend the foundational principles that ensure peg stability and facilitate yield generation.

USDe Price Stability

The fundamental purpose of a synthetic dollar is to be stable and remain pegged to the selected asset, in this case, USD. Ethena ensures USDe stability by executing an automated delta-neutral hedging strategy relative to the underlying collateral assets. Unless you’re steeped in quantitative finance, chances are those fancy terms are flying over your head. Don’t worry, we got you covered.

Hedging in finance refers to the practice of using financial instruments or strategies to reduce or mitigate the risk of adverse price movements and protect against downside risk. It involves taking positions that offset potential losses to minimize them. As previously mentioned, and frankly, as the name suggests, Ethena is an Ether-backed synthetic dollar. This means that without any form of hedging, the protocol would be directly exposed to the price fluctuations of ETH, which, as one can imagine, is not a desirable feature for a stable asset. Consequently, for the Ethena system to function effectively, it’s necessary to implement a hedging strategy for Ether’s volatility. Ethena accomplishes this by establishing a corresponding short perpetual position on a derivatives exchange, matched in value to the Ether collateral, to mitigate this exposure. Perpetuals require a margin – collateral that allows the exchange to liquidate the trader if the trade moves against him.

Delta hedging focuses specifically on the risk tied to price fluctuations of the underlying asset, in this case, ETH. It represents a more refined and targeted method within the overarching strategy of hedging. Given that USDe is a synthetic dollar, it aims for a delta of zero, achieving a delta-neutral stance. This concept, prevalent in options trading, ensures that the total delta of the portfolio equals zero. The recipe for USDe equals:

1 USDe = $1 of ETH + Short 1 Ethereum / USD Inverse Perpetual

Minting 1 USDe requires 1$ of ETH and ETH/USD short perpetual position worth $1 of ETH. To access the most liquid contracts, Ethena utilizes centralized exchanges and must provide collateral to open derivative positions and execute a peg stability mechanism. Ethena collaborates with several Off-Exchange Settlement providers that custody deposited assets and delegate/undelegate assets to/from centralized exchanges without ever transferring the assets to the exchanges. Minting occurs when:

- User deposits a selected crypto asset, LST or stablecoin, into the Ethena protocol.

- Protocol moves assets into wallets accessible by the provider.

- Off-Exchange Settlement providers deposit assets into derivatives exchanges.

- Ethena opens a short ETH/USD position.

- Ethena mints an equivalent amount of USDe and transfers funds to the user.

It’s important to note that users depositing assets receive USDe minus any costs incurred to execute the hedge, including slippage and execution fees. These costs are factored into the price when minting or redeeming USDe. Given the current gas prices on the Ethereum network, this makes the process less favorable for small amounts of collateral.

Off-Exchange Settlement providers enable frequent settlement and mitigate any potential exchange failure consequences. The price stability mechanism in practice includes the following steps, considering the ETH price falls:

- We have 1 ETH as a margin

- ETH price decreases from $1 to $0.1

- The value of the ETHUSD short position increases $1 / $0.1 = 10 ETH

- The ETHUSD position PNL is 10 ETH – 1 ETH = 9 ETH

- Our total balance is the initial margin 1 ETH plus profit from the ETHUSD position 9 ETH, equalling 10 ETH

- Now, holding 10 ETH valued at $0.1 each, we keep our balance constant at 10 * $0.1 = $1

The peg stability mechanism works correspondingly in the opposite event of the ETH price increase. For more examples, head to Ethena documentation. Thanks to measured collateral management and delta-neutral hedging, USDe remains pegged 1:1 to USD. Moreover, even crypto markets are not entirely efficient, which means arbitrage opportunities are present. This serves as another mechanism to help maintain the synthetic dollar’s peg. Market participants can capitalize on the price discrepancies between different centralized and decentralized markets. By leveraging these differences, they help narrow any gap in USDe’s price from the $1 mark.

Mighty Yield, Is It Sustainable?

The Ethena protocol produces native yield, providing USDe with an advantage over the most popular stablecoins. Ethena incorporated two primary income streams: staked ETH and perpetual swaps spreads and funding. ETH yield consists of three main avenues:

- Inflationary rewards from the consensus layer,

- Fees from the execution layer and,

- MEV capture.

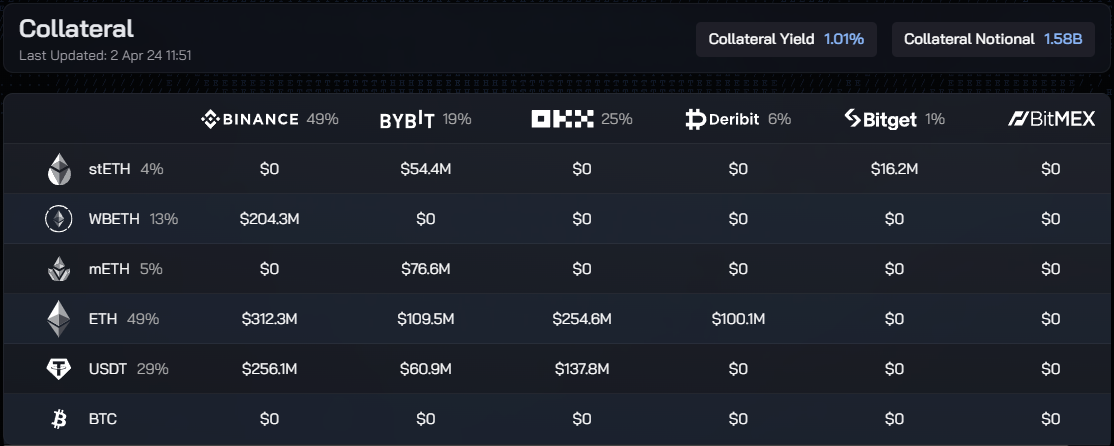

To harness the aforementioned yields, Ethena leverages external liquid staking services by enabling the deposit of tokens like stETH, WBETH, and mETH. Perpetual swaps generate income through funding rates, which are payments made between traders based on the difference between perpetual contract prices and the underlying asset’s spot price to ensure the contract tracks the spot price closely. Ethena strategically maintains short positions to safeguard against fluctuations in the USD value of staked ETH. The expectation is to benefit from positive funding rates, stemming from ETH’s deflationary characteristics and the potential for USD inflation, which, according to an analysis by Ethena Labs, has predominantly been the case, averaging between 6% and 7.5% over the past three years (Source).

ETHUSD perpetual should trade at a premium to the spot ETH (contango), ensuring positive funding. Ethena yield mechanism relies on two sources considered as improbable to change. However, the turning tables possibility persists, which will be described in the Risks section.

Both yield streams are subjected to APY changes. Accurate predictions of Ethereum’s staking yield are unattainable due to the multifaceted nature of the dilemma and the constantly evolving conditions of the network. Funding rates also fluctuate, governed by the laws of supply and demand. Ethena leverages a range of leading centralized exchanges and spreads its collateral to mitigate exposure and seize the highest yield.

Staked USDe Or Simply sUSDe: The DeFi Version Of USDe

USDe underlying mechanics and yield generation led to the Internet Bond creation. It blends the stability found in stablecoins with the censorship resistance characteristic of cryptocurrencies like ETH and its derivatives in the form of LSTs. Users can stake their USDe to obtain sUSDe, granting access to the protocol’s generated yield. Consequently, USDe could become a vital reserve asset for DeFi applications in search of stable, yield-generating collateral, as well as a ubiquitous medium of exchange that meets the high return expectations of crypto natives.

Hayes, along with a significant part of the crypto community, sees the potential for Ethena and USDe to grow exponentially from this point, with some even daring to dream that it could eventually surpass Tether as the largest stablecoin. Ethena’s promise stems from its novel method of synthetic dollar issuance and its autonomy from conventional banking allies. Contrary to Tether and similar fiat-collateralized stablecoins, which grapple with regulatory hurdles and depend on conventional financial go-betweens, Ethena conducts the majority of its activities on a public blockchain, offering a transparent and decentralized alternative.

Staking USDe and acquiring sUSDe grants access to protocol rewards without requiring any further action from users. sUSDe is a reward-bearing token that appreciates over time, akin to swETH or rETH. The value of rewards is tied to the exchange rate between the derivative token and the staked asset. sUSDe holders are assured of receiving a yield of >= 0%. The value of sUSDe is designed to remain stable, even in scenarios where the protocol faces negative yields since the assets are locked in the staking contract and cannot be withdrawn. Should there be any losses, they are expected to be covered by Ethena’s Insurance Fund (Source).

Ethena Protocol Performance

Ethena really hit the ground running with USDe. From day one, the product has been a success story, attracting hundreds of millions of dollars and tens of thousands of users. The unprecedented yield levels for a product marketed as a synthetic dollar, combined with a well-structured points campaign, played a crucial role in the success of the venture. Market conditions favor high yields generated from both sources. Funding is positive, and longs pay shorts interest, aligning with the protocol’s objective. ETH and LSTs rewards also influence the APY. Although staking base APR decreases, ETH stakers receive rewards associated with network fees, which have been elevated recently. The recent Dencun Ethereum upgrade lowered gas prices on Layer 2, but the wave of new users flowing in during the bull market will push transaction costs even higher.

Ethena Labs introduced the Shard Campaign to boost the adoption and incentivize new users to deposit their assets. These points represent and track users’ involvement in the Ethena ecosystem throughout the campaign. This approach has become table stakes for new protocol launches recently and has proven effective in boosting TVL and community growth. However, it’s worth noting that Ethena has maintained its uniqueness with interesting community dynamics. Ethena capitalized on the campaign, attracting over 41k users.

Ethena rolled out its public version approximately a month ago, and since then, its TVL has absolutely soared. The collateral locked in the protocol now totals $880 million and includes various positions such as ETH, USDT, stETH, WBETH, and mETH. USDe supply equals $882M, ranking it 6th among stablecoins. It has surpassed FRAX, crvUSD, or PYUSD already, and it is just a matter of time before USDe will fight for a Top 3 spot.

$ENA Token Governing The Ethena Protocol from 2nd April 2024

Ethena announced the launch of its native token $ENA on 27th March 2024. It was the first step in decentralizing the Ethena protocol and a move towards the team’s vision of Internet Money. The airdrop concluded the 6-week-long Shard Campaign, which was one of the shortest pre-token campaigns back then that incentivized the growth of USDe supply to a whooping $1.35bn. The impressive growth made USDe the fastest USD-denominated asset to reach >$1bn supply ever in crypto at the time of writing.

The conclusion also meant that 5% of the $ENA supply was airdropped to users. The sunsetting of one program became also the beginning of the second one called Sats Campaign.

Risk

Ethena offers a novel approach to synthetic dollars, pairing it with yield generation. As the protocol was launched recently, it hasn’t been battle-tested yet, and some of its mechanisms might introduce risks. The concern that has garnered the most attention revolves around how the protocol would operate under prolonged periods of negative funding rates. There exists a scenario where negative perpetual swap funding rates could potentially cause USDe to deviate from its peg to the downside.

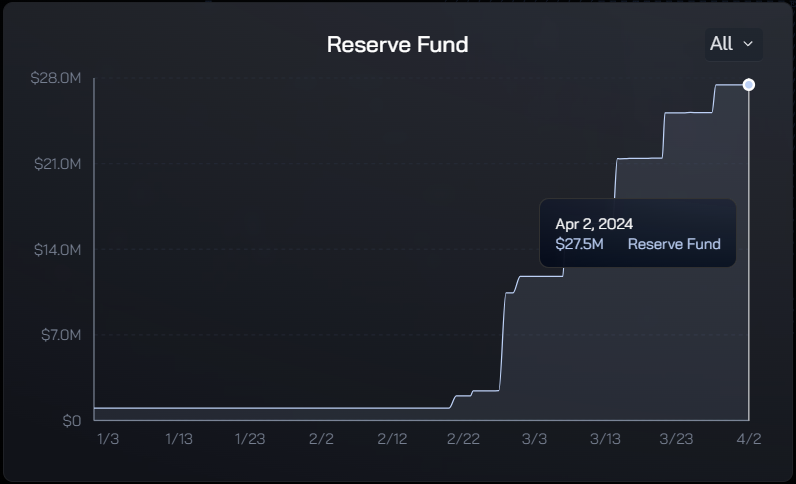

The ReserveFund would be deployed in case of such an event. It serves as an additional safety measure behind USDe, providing capital to cover periods of negative funding and acting as a buyer of last resort for USDe in open markets. It comprises uncorrelated collateral such as stablecoins (USDC, USDT), smaller allocations of staked Ethereum (stETH), and liquidity provider positions in USDe and USD. The fund’s capitalization comes from a portion of the yield generated by the protocol’s asset backing, funds raised from investors, and a long-term take-rate on generated yield.

Ethena is exposed to counterparty risk from derivative centralized exchanges where it holds short perpetual positions. If these exchanges fail to pay out profits or return deposited collateral, Ethena could suffer capital loss. Although unlikely, Ethena could face liquidation if the value of staked ETH collateral diverges significantly from the value of the short derivatives positions. In addition, LSTs utilization as collateral poses risks related to liquidity and loss of confidence in the integrity of LSTs due to smart contract and protocol flaws. Should Lido face a downturn, this would impact stETH, consequently diminishing its value.

Furthermore, Ethena is exposed to custodial risks, relying upon providers to custody assets and manage CEX exposure. The risk of slashing exists, penalizing Ethereum node validators and their underlying ETH stake. Last but not least, the circulating supply of USDe is limited by the total open interest of Ethereum futures and perpetual contracts, hindering Ethena’s ability to grow without limitation.

Resources

- https://ethena-labs.gitbook.io/ethena-labs/

- https://app.ethena.fi/

- https://blog.bitmex.com/dust-on-crust/

- https://blog.bitmex.com/dust-on-crust-part-deux/

About RedStone

RedStone is a modular blockchain oracle delivering diverse, high-frequency data feeds to EVM Layer1, Layer2, Rollup-as-a-Service networks, and beyond, i.e., Starknet, Fuel Network, or TON.

By responding to market trends and developer needs, RedStone can support assets not available elsewhere. The modular design allows for data consumption models adjusted to specific use cases, i.e., capital-efficient LSTfi and early support of LRTs. RedStone raised almost $8M from Lemniscap, Blockchain Capital, Maven11, Coinbase Ventures, Stani Kulechov, Sandeep Nailwal, Alex Gluchovski, Emin Gun Sirer, and other top VCs & Angels.